ASML Q2-26 Earnings Preview

Quick look into what I'm watching tomorrow.

ASML is supply-constrained, not demand-constrained

Good morning to you all,

As some of you might know, ASML is my biggest holding and also one of my highest conviction positions. Therefore I’m always very exited when they report earnings.

Usually, they do not disappoint.

Tomorrow ASML will report their Q2 earnings.

First, the market’s expectations:

EPS is expected to come in at €6.9, which would be 17% YoY growth and a 6% QoQ decline.

Total net sales: €8,879B which would be 15% YoY and 1% QoQ growth.

ASML guided for:

Total net sales between €8.4B and €9B

Gross margins between 51% and 52%

I think they should be able to meet those estimates quite easily, but what’s more important is their guidance.

ASML has kept their 2030 guidance unchanged between €44B and €60B for years now. Personally I think this is way too low for what the market is pricing in today.

Bernstein recently raised their 2030 outlook to €80B, and believes that with that growth a higher multiple is also warranted. They argue the stock is cheap as of today.

With everything happening in the memory sector right now, I too believe that the 2030 range that ASML uses is too low. However, I still think ASML will continue to lean conservative, until we get closer to 2030. A guidance upgrade would really cement everyone’s outlook, but ASML is notoriously known for being very conservative with their guidance and forward looking statements.

It’s crystal clear that demand for ASML’s machines is sky-high right now. That’s not the problem. The problem will be ramping up and getting these machines installed properly and timely at their clients.

I do think ASML will ramp up the speed at which they will deliver these machines. They have to.

Usually they ship between 70 and 80 lithography machines, but I expect this number to increase significantly over the next few quarters.

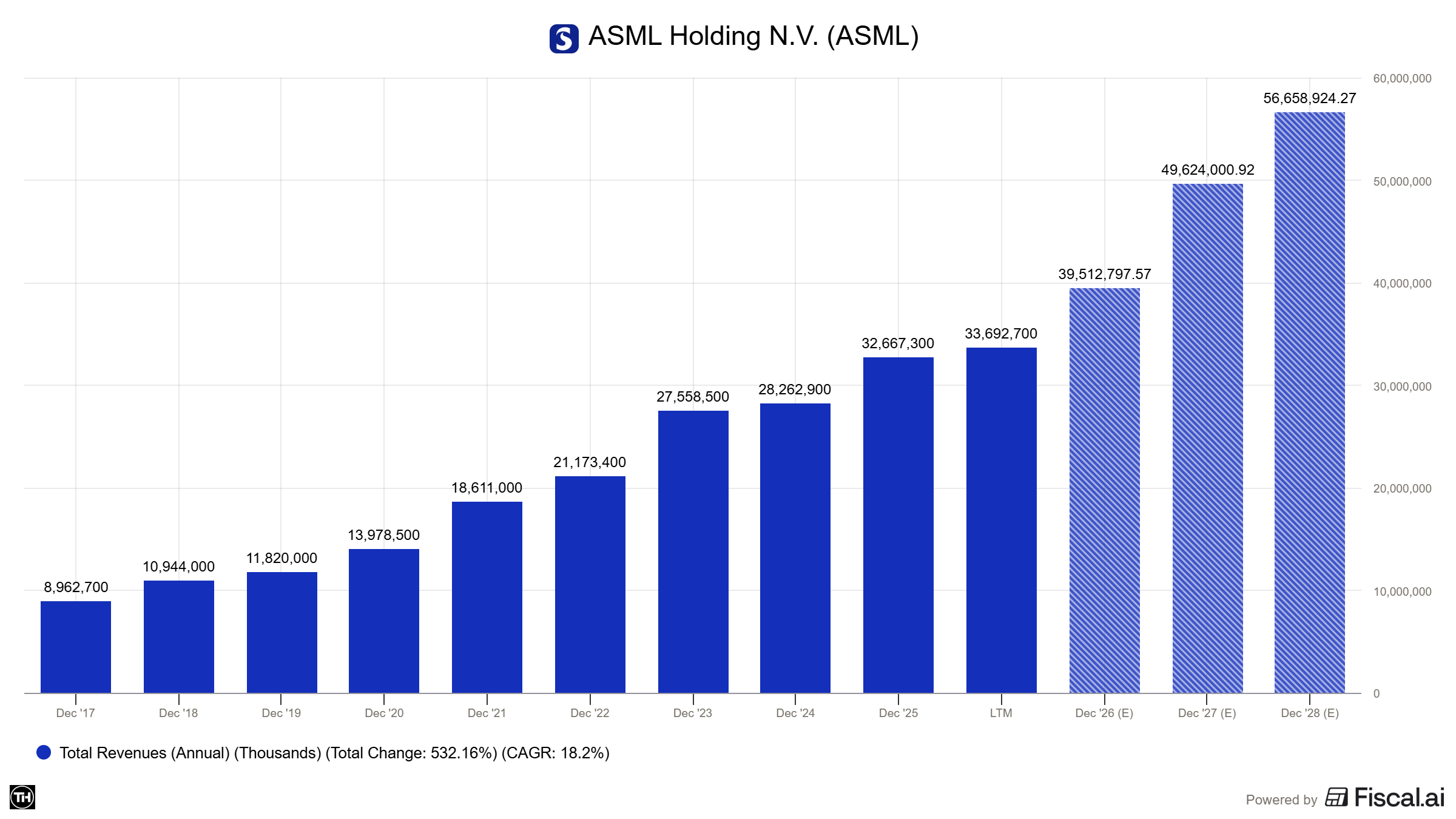

Bernstein also thinks the EUV section could grow 30% CAGR from here, and reach €43B by 2030. Looking at fiscal.ai analyst forecasts, a similar picture arises. They expect ASML to do €57B in revenue in 2028, which would already be close to the upper range of ASML’s 2030 guidance.

Overall, it’s clear the demand is picking up. ASML is one of the key players to watch, as a lot of the growth potential of their clients, like TSM, Hynix, Samsung and Micron revolves around the ability of ASML to ship their machines in time.

My personal expectations:

Guidance increase for FY2026. I think a range of €37B tot €41B is in the cards

Guidance increase for 2030. Maybe they’ll be conservative again and keep 2030 guidance unchanged, but I believe a new range of €48B to €64B for 2030 is realistic.

Margin stabilization at 52% gross.

Some other points I am watching:

The roll-out of High-NA EUV. More High-NA revenue is expected to be recognized in 2026. But all well depend on whether customers are actually qualifying the tool for production or just running R&D on it.

Hints at 2027: for now they just frame it as a growth year, but I hope they can actually tell us what that growth trajectory might look like. This matters more than it used to, because ASML stopped reporting quarterly net bookings to reduce stock volatility. So we need management to properly guide us going forward

China: Is China backlog still intact and is DUV-to-China is stabilizing or still bleeding

ASML is a derivative play on its customers' spending. If AI is genuinely forcing leading-edge expansion, ASML captures it.. DRAM/HBM capex is ramping hard. If ASML can facilitate the growth wishes, that would be a large new wave of demand. It certainly looks like this is realistic.

An increase in gross margins would be welcome. High-NA units are lower margins as of now, but if all the other segments increase faster than expected, we could also se higher margins.

Capacity: I would love some numbers regarding output. For now they said "at least 60" Low-NA EUV systems output for 2026.

The forward looking story is clear. For ASML it’s about making sure there’s enough capacity for customers. It’s not about whether demand shows up. It’s about whether ASML can build enough. ASML is building as fast as customers will commit to, and customers are sold out.

With the share price being up 125% in a year, they will have to show good numbers.

I think they will do just that.

Gonna be a fun day tomorrow!

If I have the time I will write an earnings review this week.

Cheers,

TacticzHazel

Disclaimer

The content I share is for educational and informational purposes only. It should not be considered financial, investment, or trading advice. All opinions expressed are personal views and are not guarantees of future performance. Investing involves risk, including the potential loss of capital, and past results do not indicate future returns.

Before making any investment decisions, you should conduct your own research or seek guidance from a licensed financial advisor. I am not responsible for any financial outcomes resulting from actions taken based on the information provided.

By engaging with this content, you acknowledge and agree that you are solely responsible for your own investment choices.