DLO - Q4 Earnings - Quick thoughts

Dlocal just reported earnings. I don’t really care what the market says or does, but I’m impressed.

They beat both on revenue and EBITDA.

Revenue of $337.9M vs. $296.1M est.

Adj. EBITDA of $78.4M vs. $76.9M est.

Most important metrics to watch usually are: TPV, Revenue, Margins and Gross profit.

And of course we will have a look at the take rates as well, as that’s what a lot of investors worry about usually.

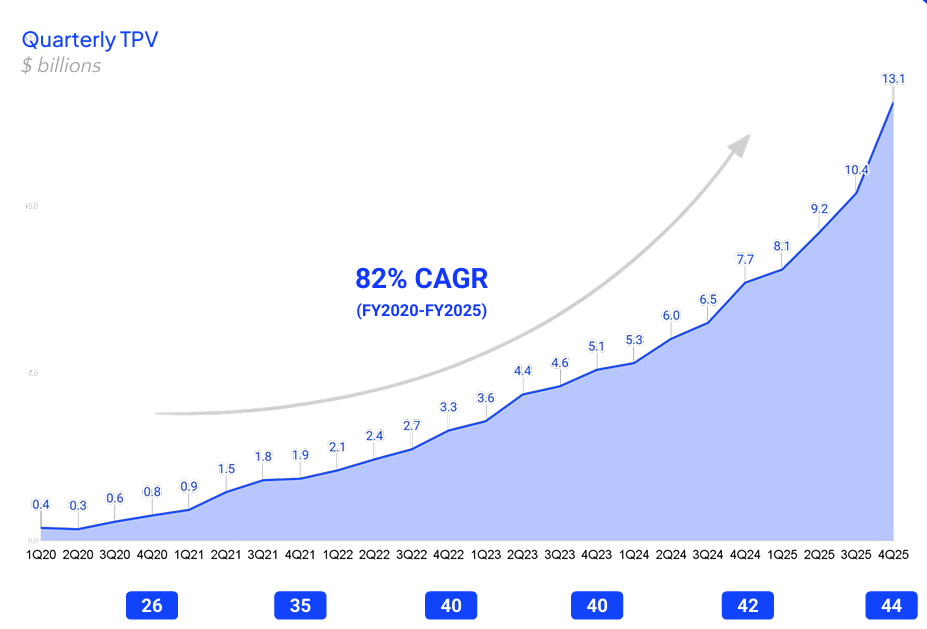

TPV reached $41B, up 60% YoY, with 5 consecutive quarters of >50% YoY growth and accelerating in the 2nd half of the year. This growth is just something else.

Revenue surpassed $1B (came in at $1.1B)

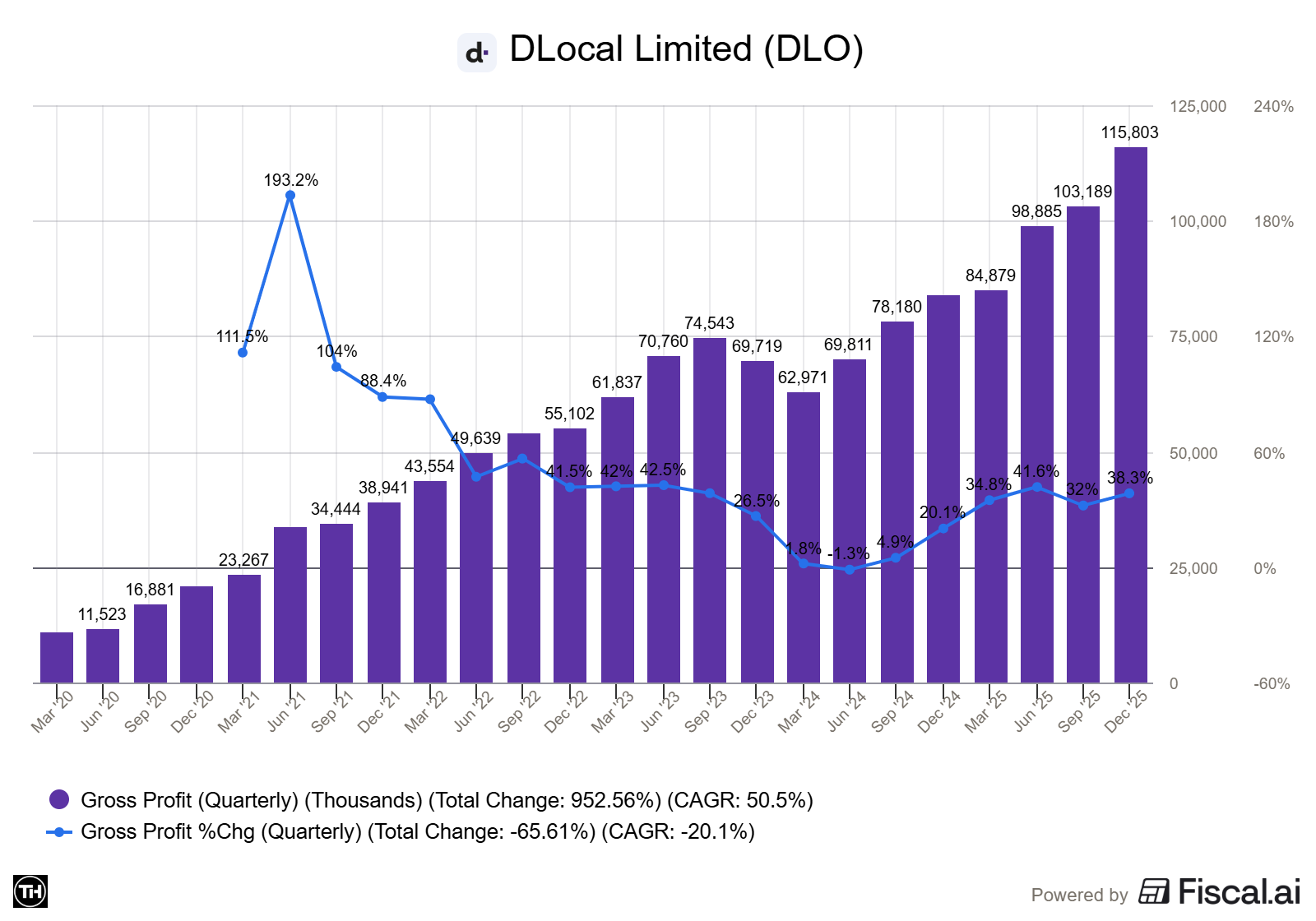

Gross profit reached $403M, which is a +37% YoY

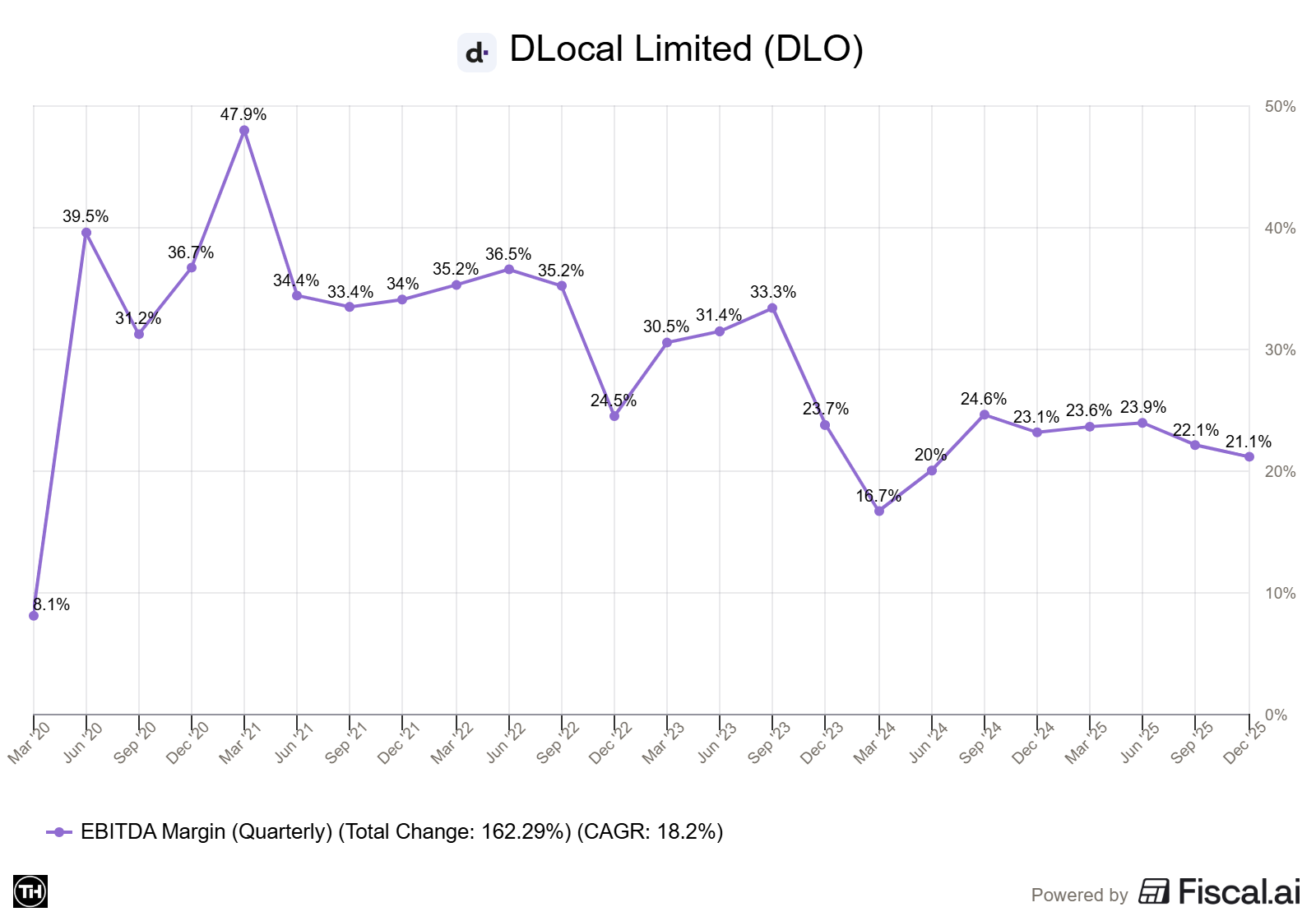

Adjusted EBITDA up 47% YoY with significant margin improvement (+5 p.p. in Adj. EBITDA1 / Gross Profit) despite being in an investment year

Net income up 63% YoY to $197M

Adj FCF1: $191M; forthcoming dividend payment of $57M

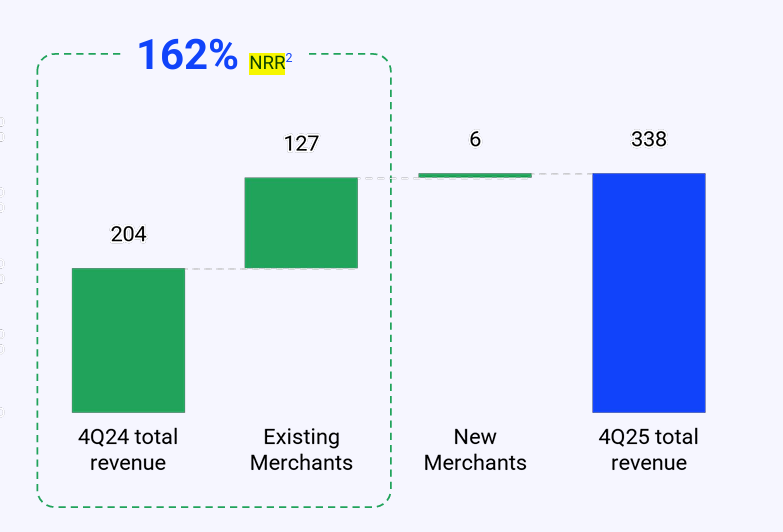

Net revenue retention of 145%

More importantly guidance shows a similar trajectory for 2026.

The guide for:

TPV —> between 50% - 60%

Gross profit —> between 22.5% and 27.5%

Operating profit —> between 27.5% and 32.5%

So, let’s calculate the measure everyone is always so worried about.

Normal take rate = Revenue / TPV —> $1.093B/ $40.816B —> 2,68%

Net take rate = Gross profit / TPV —> $403M / $40.8B —> 0,99%

Last quarter the normal take take rate was 2.72%, so that’s a slight decline. But nothing major and also nothing to worry about in my opinion.

The net take rate sits at 0.99% which is the same as last quarter. Nothing new there. I do not expect an increase there anytime soon. Stagnating is what we aim for.

They also announced a share repurchase program of $300M. They sit at a lof of cash and this is probably the best way to use it right now. Scaling doesn’t require a lot of investments, so they can put the cash to work via dividends and buybacks.

Another important metric is the NRR. This stands for Net Retention Rate.

This metric measures both how well DLocal retains its existing customer base and how much additional revenue it gains from those clients over time.

The NRR came in at 162% compared to 136% last quarter.

This is what we wanna see. Continued strong growth, with a stagnating decline in take rate.

They only two things to continue watching:

Margins are still in decline and gross profit is stagnating.

Gross profit used to be above 30%+, but now they guided between 22.5% and 27.5%. This is not a decline we want to see.

EBITDA margins are still above 20%, but in decline still, now at 21.1%

That’s the little snapshot for now. Overall, I’m impressed and this is another great quarter.

I’m sure there are things to worry about, but that might take a bit more time to really find out.

I wont be making a full earnings breakdown, as I’m finishing some other articles that I want to get out first.

If you have any questions, feel free to shoot.

Cheers,

TacticzHazel.

What an incredible chart, wow.

The TPV growth is stunning