Dlocal (Deep Dive)

A highly asymmetric bet on the rise of Emerging Markets.

1. Introduction

Dlocal, is a company that deserves a lot more attention than it currently gets. It’s fast-growing, has tons of secular and region-specific tailwinds, a strong management-team and a fantastic scalable business model.

One of the things that has led me to put Dlocal high on my deep dive list, is the asymmetric opportunity I believe it provides right now. Downside is limited due to attractive valuation, and the upside potential is huge.

DLocal is well positioned to benefit from the rapid rise of Emerging Markets and their recent growth story shows this.

In this deep dive I will unpack everything you need to know about Dlocal. I cover the most important parts of the business and end with the valuation model.

As always I will approach this in the most objective way as I can and highlight the good and the bad.

Disclaimer: I do have a position in Dlocal right now.

Let’s dive in!

This isn't something I normally ask in the beginning of the post, but if you found this deep dive valuable and you enjoyed it, please like and share this post and consider subscribing. It helps me tremendously and ensures that as many people as possible see my work.

I also run a 50% discount right now if you want to become a paid subscriber. This means you’ll be able to get access to all of my private content and get access to my discord group for only €11.50p/m or €8p/m on the yearly plan

2. The opportunity

So let’s first start with why this opportunity exists. I believe Dlocal is still not being fairly treated by the market. The last couple of years have been challenging on many fronts, but if you look past the headlines, there’s a gem hiding in plain sight.

The short-reports from a couple of years ago still hang as a negative blanket over the company and scares investors to hop in. But while some of the arguments were not completely unfounded, the main arguments have been proven to be completely false.

All the while, the company has taken some of the critique to heart and they have made some drastic changes that have improved the company’s foundation. This has led to one of the fastest growth stories in the online payment sector, partially driven by the appointment of a new CEO. But for some reason this company is still flying under the radar for many investors.

Companies related to emerging markets are still not given the praise they deserve, and are still frowned upon and underowned. To me, that’s unjustified, and I think in the upcoming years a lot of value will be unlocked in these EM-plays as they get valued appropriately.

Some numbers:

5 year revenue CAGR: 68.3%

Gross margin: 38.6%

Net margin: 18%

Forward P/E: 16.3

Strong cash position/ almost no debt

Forward looking:

Revenue forward 2 year: 35.1%

EBITDA forward 2 year: 38.9%

EPS forward 2 year: 47.8%

I do want to point out, that while this growth story looks spectacular on first sight, investing in Dlocal does not come without risk. This is a high-growth company, that’s scaling fast. There are definitely execution risks, and some other headwinds that I will explain later in the deep dive. But then again, there’s risk investing in every company!

So, let’s first find out how Dlocal started.

3. Dlocal as a company

3.1 Origin story

Dlocal was founded in 2016, but the origin story goes back a bit further, to 2009. Dlocal’s co-founders Sergio Fogel and Andrés Bzurovski started it all with a company named Astropay.

AstroPay started in Uruguay in 2009 and basically operated as a prepaid virtual card and online payment solution for users who didn’t have credit cards, mainly in Latin America. It grew rapidly, mostly by enabling cross-border payments for global merchants, with a strong focus on gaming, e-commerce, and digital services.

The business was quite successful and that led to a spin-off: a separate company focused on enterprise cross-border payment processing in emerging markets, you guessed it: Dlocal.

AstroPay remained more of a ‘‘consumer wallet’’. I think it’s safe to say that AstroPay proved the payment model with consumers first and then in turn dLocal evolved from that model into the global B2B payment giant it is today.

DLocal was founded with a a very simple goal: to make online payments easier for global companies selling in emerging markets. They noticed a very clear and major problem in these markets: large international business wanted to go there and grow, but the local payment systems were very complex, hard to grasp and totally inefficient. Dlocal wanted to lift that barrier and give these large business better access to these markets.

There was no usable infrastructure for emerging markets, so Dlocal decided to built it themselves. They began very small, with just one product, one payment method in one country, Brazil. After the successful start in Brazil they got hungry for more and they took this experience to expand to other countries and regions. Now, they operate in Latin America, Africa, and Asia and they cover over 40 countries. The most noteworthy are: Brazil, Mexico, Argentina, Colombia, Chile, Nigeria, Egypt, South Africa, Morocco, India, the Philippines, and Indonesia.

From the start, there has been a strong focus on scalability in Dlocal. They created a flexible and scalable system that was ‘‘easily’’ able to grow along with their customers. In theory it was very simple, built a strong foundation and then add new layers and solutions based on what the consumer wants and needs. This flexibility leads to a high adaptability in this fast-changing payment ecosystem.

DLocal’s first big win came from modernizing Brazil’s Boleto payment system. Instead of requiring customers to print a payment slip and pay in person, the company enabled Boletos to be generated and paid digitally at checkout. What initially seemed like a Brazil-specific solution revealed a much larger opportunity: fragmented payment systems across emerging markets in Latin America, Africa, and Asia.

Now, when global companies are pushing more and more of their business into Emerging Markets, demand for DLocal’s services is growing fast. The platform evolved from supporting just a single payment method to integrating hundreds of local options through one unified API, making cross-border expansion far simpler. That’s what makes Dlocal unique, but more on that later.

On June 2021 Dlocal IPO’d on the Nasdaq, They went public at $21/share, valuing the company at ~$6 billion. It became Uruguay’s first high growth private company to list on a major US exchange

A turning point came when GoDaddy became its first major U.S. client. After an early attempt at a consumer prepaid card, DLocal realized enterprises wanted infrastructure, not another wallet brand. This led to a full pivot to a B2B model, which in turn unlocked rapid global scaling and long-term enterprise partnerships.

In 2022 they began aggressive hiring in Africa, scaling its operations to process payments in major hubs like Nigeria, South Africa, and Kenya.

And then came the short reports.

3.2 The short reports

When investing in Dlocal, it is important to know the sentiment history around this company, it wasn’t good for many years. And that’s due to short reports.

The most important one, was the one from Muddy Waters. Muddy Waters published a bearish report accusing dLocal of financial irregularities, misleading disclosures, weak controls over client funds, inflated metrics, and governance issues, and took a short position betting the stock would fall as a result. dLocal rejected the claims as inaccurate.

It took some time for Dlocal to overcome this negative sentiment. But with some leadership changes (Pedro Arnt became CEO in 2023) and strategic refocusing, there now seems to be a shift towards fundamentals, over sentiment and short reports.

Some of the issues that were raised had elements of truth, and Dlocal addressed them. They focused on improving their accounting efforts (which can be tough in the complex environment they operate in) and reduced exposure to certain high-risk endeavors. All in all, I think it made them fundamentally stronger.

But this is what you should remember: The most severe accusations (like fraud and fabricated revenues), were never proven.

Many other short reports followed (like the one from Spruce Point), but those were mainly just echoing what Muddy Waters already tried to ‘‘expose’’. In the end, a lot of noise, and not so much actually proven.

But then again, if I tell you now to not think about a pink elephant, that’s exactly what you’ll be thinking about. And that also happened to Dlocal, and it still casts a shadow over the company till this day. Unrightfully so in my humble opinion.

4. Company structure + overview

4.1 The parent company

DLocal Limited, which is the the publicly traded parent company is incorporated in the Cayman Islands. DLocal Limited was established as a limited liability holding company in Malta. In 2021, it was reorganized under dLocal and domiciled and incorporated in the Cayman Islands. The Cayman Islands entity functions as a holding company, which owns dLocal’s operating subsidiaries around the world.

I always raise my eyebrows when I see the name ‘‘Cayman Islands’’, as I immediately relate it to money laundering and financing of terrorism. However, after doing some digging it’s actually quite ‘‘normal’’ for tech and fintech companies to incorporate in the Cayman Islands because of:

Tax neutrality

Investor-friendly corporate law

Ease of international capital raising

Common structure for U.S.-listed foreign companies

So, not a red flag for me, but it did stand out a bit.

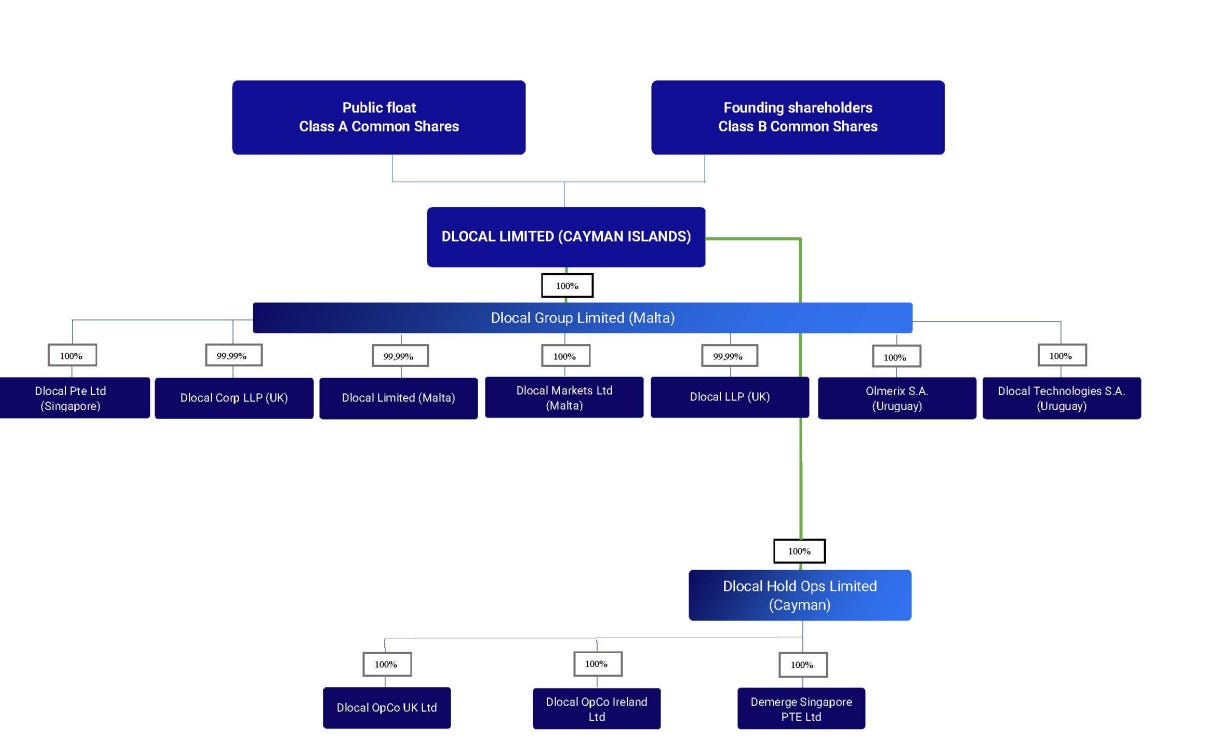

4.2 Corporate structure

Below is an overview of Dlocal’s corporate structure. Dlocal limited is the corporate entity on top, with all it’s subsidiaries like Dlocal Corp LLP and Dlocal Markets underneath.

As of December 31, 2024, they had a total of 285,475,136 common shares issued and outstanding. Of these shares, 134,054,192 are Class B common shares, owned by shareholders that have held these shares since prior to the IPO and 151,420,944 of these shares are Class A common shares. Dlocal holds 18,754,887 Class A common shares as treasury stock.

5. Management

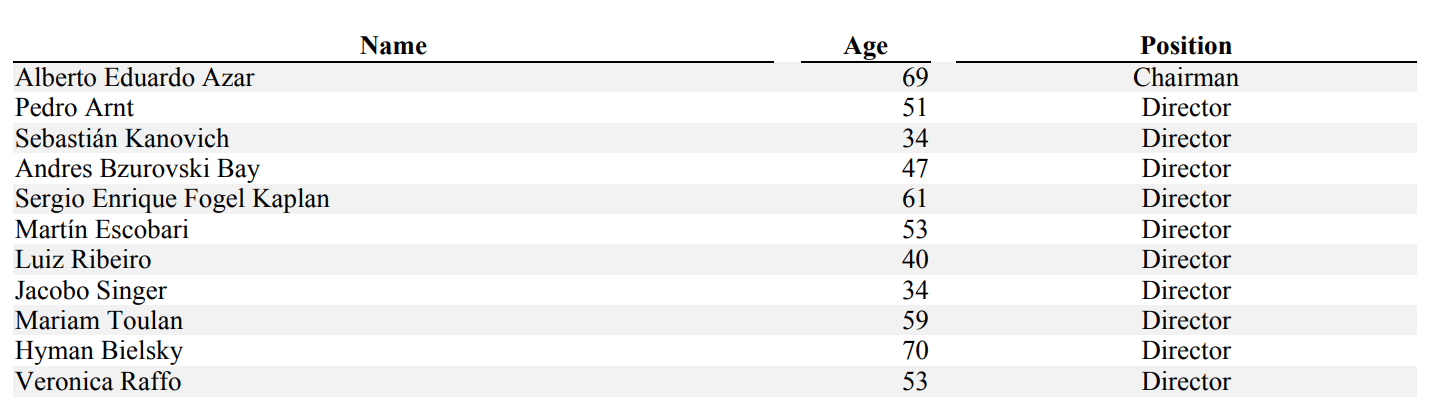

5.1 Board of Directors

Dlocal is managed by it’s board of directors and senior management. This is an overview of the board from the annual report of 2024.

There have been two major changes since:

Will Pruett was appointed to dLocal’s Board of Directors (and to the Audit Committee) as of July 1st

Mariam Toulan ended her term on June 30th

Will Pruet has a long and wide background in emerging markets and capital markets so this might suggest that dLocal is strengthening its governance and possibly preparing for further growth or capital-market activity.

Overall, this is a very experienced board with lots of sector and EM-knowledge.

5.2 Pedro Arnt (CEO - Chief Executive Officer)

Pedro Arnt is one of the main reasons why I started looking into Dlocal. He is an incredibly experienced and knowledgeable CEO. Pedro is a rare combination of being extremely smart, having a hands-on mentality, but also a class-act in the way he treats people and conducts his interviews. You can tell he has a high level of maturity in his business approach and a strong focus on long-term thinking.

Before joining Dlocal he was Chief Financial Officer and Executive Vice President of MercadoLibre for more than twelve years. Before joining Mercado Libre, he worked for The Boston Consulting Group.

Pedro Arnt joined Dlocal in August 2023, and was appointed CO-CEO next to the co-founder Sebastián Kanovich. Kanovich no longer leads day-to-day operations as CEO, but stays heavily involved at the strategic level via the board and by heading commercial and M&A oversight. Arnt is now sole CEO.

This was not a forced decision, and Kanovich truly thinks Pedro Arnt is the right fit for the company, as he said:

Going nowhere, going to the board. I love this company too much, I’m going to still be around. We’re establishing a commercial and M&A committee that I’m going to be leading. But it’s time for me to step down as CEO, it’s been a huge ride and an incredible one but as a public company and looking ahead, I think Pedro is in much better position to do it. I’m going to be supporting the company, but from one step behind, which is a place I feel a little bit more comfortable with as well.”

Arnt described joining dLocal as;

‘’a unique chance to scale a company that’s “big enough to do amazing work, yet still innovating and building’‘

Pedro played a crucial role in scaling MercadoLibre from a startup to the huge company it is now with a market cap exceeding $100B. His aim is to do something similar with Dlocal.

What must not be underestimated is how well a CEO fits, with the current stage a company is in. Pedro did not choose Dlocal by accident. Pedro has deep understanding of Latin America’s technological ecosystem, but more importantly he has a very outspoken passion and natural affinity for the scale-up stage of companies.

That’s where he truly shines and where he believe he can make a big difference. He did this at Meli, and therefore in the current stage Dlocal is in, he seems like a perfect fit. And investors agreed, because because when he took over as CEO, the markets reacted very positive.

Names Former MercadoLibre CFO Pedro Arnt as Co ...")

5.3 Carlos Menendez (COO - Chief Operating Officer)

Alongside Pedro we have Carlos Menendez. He brings in a wealth of experience and a proven track record in global strategic leadership and operational management, with over 30 years of experience in world class companies across payments, banking and consumer industries, including Mastercard, Citibank and Procter & Gamble.

Throughout his career, Carlos has been instrumental in scaling businesses, managing global P&Ls and leading strategic initiatives.

5.4. Jeffrey Brown (CFO - Chief Financial Officer)

Jeffrey Brown (previously VP Finance) was named interim CFO while the company searches for a permanent replacement. Mark Ortiz stepped down as CFO due to health reasons. Jeffrey Brown has only been with Dlocal for just over a year now.

He worked at Geopagos as CFO for 6 years, and before that at Axial as VP Finance and Strategy. He claims to have a particular knack for growth stage companies. He has a successful track record with arranging complex capital transactions, driving growth initiatives (including M&A), and leading financial operations.

5.5 Sebastian Kanovich (Director)

Sebastian Kanovich is widely recognized as the driving force behind DLocal’s rapid global scaling. Kanovich served as the founding CEO of DLocal from its inception in 2016 until mid-2023. Under his leadership, the company transitioned from a startup to a publicly-traded “unicorn” on the Nasdaq.

After stepping down as CEO to transition into a Board role, his function is primarily strategic oversight. As a Director, he leverages his deep institutional knowledge to advise on long-term growth, international expansion, and maintaining the company’s competitive edge in emerging markets.

5.6 Andrés Bzurovski (Chairman)

Andrés Bzurovski is one of the original visionaries behind the DLocal concept and a veteran in the fintech industry.

Bzurovski is one of the Co-Founders of DLocal. Before DLocal. As mentioned before, he also co-founded AstroPay, a global payment solution. He has been a pivotal figure in the Uruguayan tech ecosystem for decades.

As Chairman of the Board, his role is to lead the Board of Directors and ensure the company remains aligned with its core mission. He focuses on corporate governance, high-level stakeholder relations, and steering the company’s overarching vision. He acts as a bridge between the executive management team and the shareholders.

6. What does Dlocal Do?

Some things were already briefly mentioned in previous chapters, but in this chapter I’ll explain more in-depth explain what Dlocal actually does. I’ll discuss their business segments and how they actually make money.

6.1 Core business

Here is a high-over explanation of what Dlocal does:

Dlocal is a fintech company that provides payment infrastructure for global business in Emerging Markets. It focuses on making cross‑border payments feel like local payments for both the merchants and their customers.

They operate a cloud-based payments platform that lets internationally oriented businesses accept local payment methods (cards, bank transfers, wallets, cash, instant payments) and settle funds across borders. They position themselves as a single, unified API that replaces the need to integrate with many different local processors and banks in each of these countries, which can be a huge hassle with all these varying legislations and laws.

Below shows how that unified integration works.

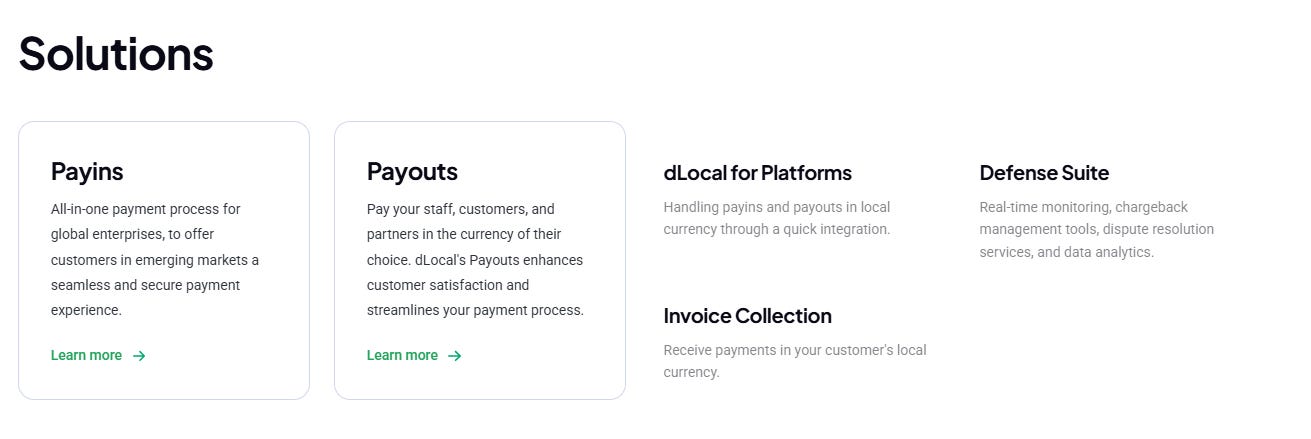

6.2 Their main solutions

So what are their main offerings? They offer 5 main solutions:

Payins

Payouts

For Platforms

Invoice collection

Defense Suite

Payins ( when customers pay a business)

Payins are customer-to-merchant payments: a shopper or user in an emerging market pays a global company using local methods and Dlocal processes and settles those funds. They accept over 700–900 local payment methods (e-wallets, bank transfers, cards, cash, etc.) in local currencies

Payouts: (when a business sends money out to people or partners):

Payouts are merchant-to-user payments: a company uses Dlocal to send money to partners, freelancers, sellers, drivers, or customers in their local currency and into local accounts or wallets.

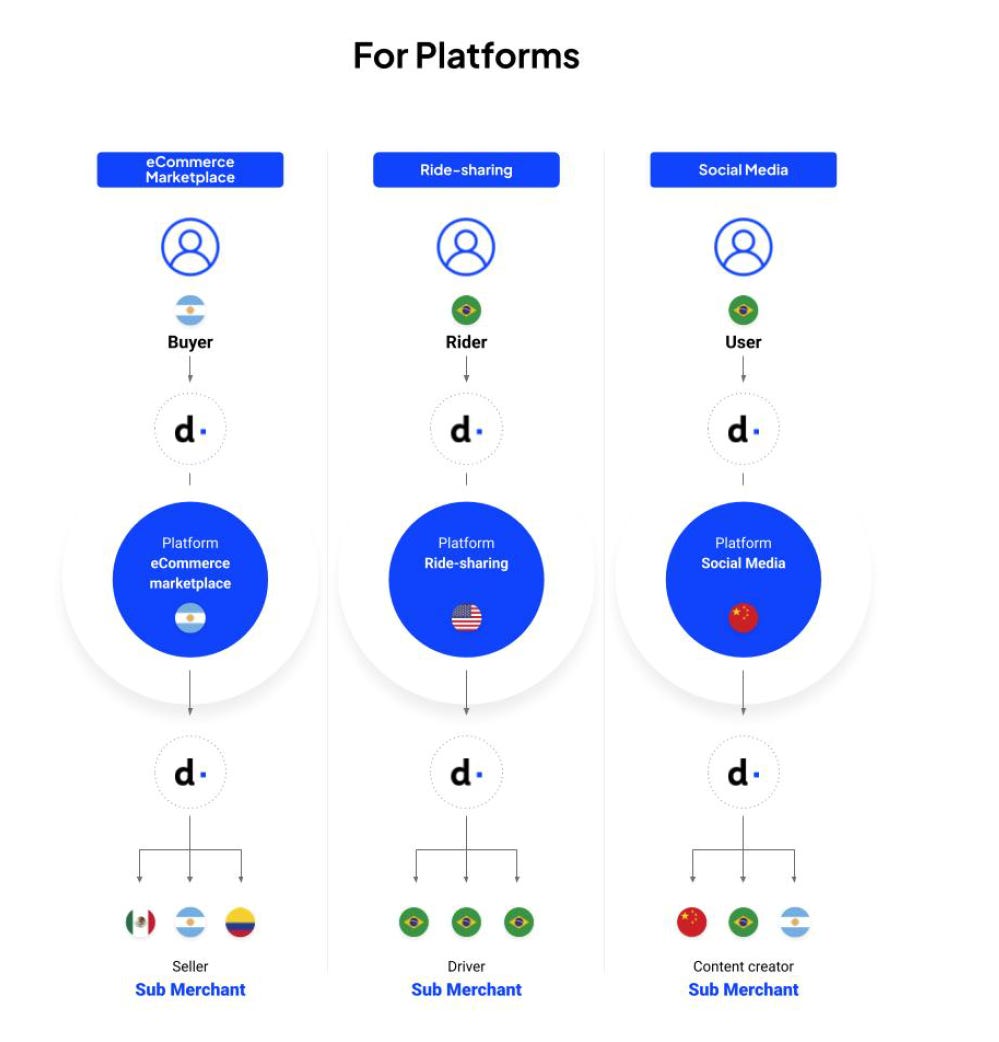

For Platforms

For Platforms is Dlocal’s solution-set for marketplaces, gig platforms, and other multi‑seller platforms that need to collect from buyers and pay out to many different recipients in multiple countries. It typically includes tools for split payments, mass payouts, reconciliation for users who are both payers and payees, and operating in multiple currencies through a single integration.

Invoice Collection

Invoice Collection is Dlocal’s product for collecting B2B or high‑value payments via invoices in emerging markets. It allows a merchant to issue invoices (often priced in a hard currency like USD) while letting customers pay in their local currency and via local payment methods, with Dlocal handling FX, local regulations, and settlement.

Defense Suite

Defense Suite refers to Dlocal’s risk, fraud, and compliance capabilities that protect payment flows. In practice, this includes fraud prevention tools (such as AI‑based transaction scoring), chargeback and dispute handling, and processes to meet KYC, AML, and local regulatory requirements while transacting across borders.

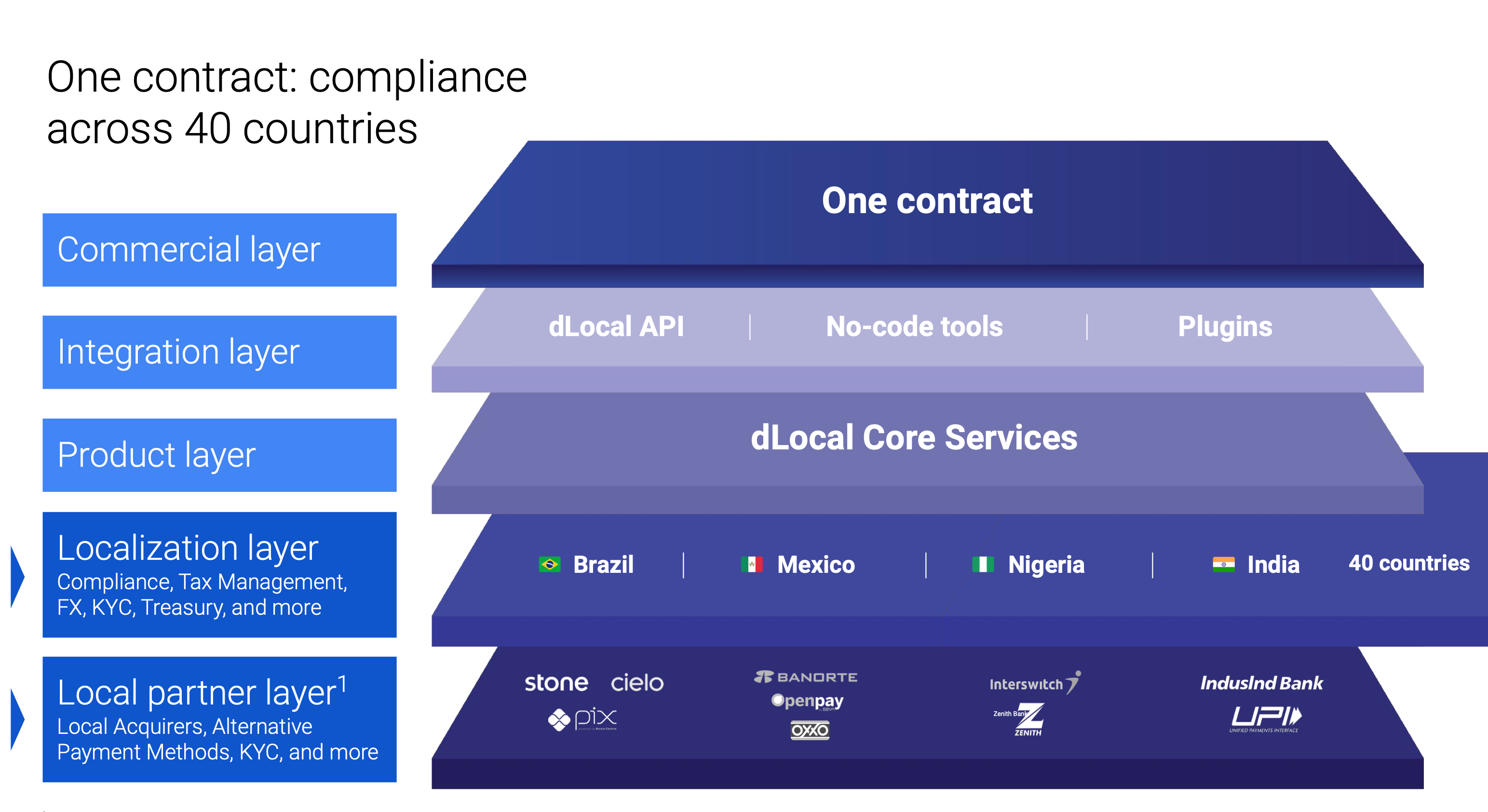

6.3 One Dlocal

They do all this through ‘‘One Dlocal’’. This basically means that they operate through One API, one platform and just one contract. This ‘‘One Dlocal’’-structure gives companies direct access to a wide variety of options, countries and payment structures.

“One DLocal” can be seen as the ‘‘core philosophy’’ and technical architecture of Dlocal. In simpler terms, it is an “all-in-one” integration that allows a globally oriented companies like Amazon, Uber or Godaddy to operate in 40+ different countries without having to build 40 different payment systems.

“One DLocal” is built on 3 main pillars, as we mentioned before:

One API:

A single technical connection. Instead of a developer writing code for Brazil’s Pix, Mexico’s OXXO, and Nigeria’s Airtel Money separately, they just connect to DLocal. DLocal’s code automatically switches to the correct local method based on where the customer is located.

One Platform:

A unified dashboard: a company can see all their sales from Egypt, Indonesia, and Chile in one place, with DLocal handling the messy work of currency conversion (FX) and moving the money back to the merchant’s home bank.

One Contract:

Legal simplicity. Instead of signing dozens of contracts with different banks and local entities in every country, a merchant signs one master agreement with DLocal and that’s it.

6.4 So, how does that work in practice?

Imagine a small business owner in Peru buying a domain name from GoDaddy. The Peruvian customer goes to GoDaddy. At checkout, thanks to DLocal, they see local options they trust, like a local bank transfer or a cash payment via PagoEfectivo.

The customer pays in Peruvian Soles. DLocal’s “One API” recognizes the transaction, processes it through the local Peruvian banking system, and confirms the payment to GoDaddy instantly.

DLocal holds that money. They handle the conversion from Peruvian Soles into US Dollars (or stablecoins like USDC), protecting the merchant from local currency fluctuations.

On a scheduled basis, DLocal sends the accumulated funds from thousands of such global transactions to GoDaddy’s headquarters in the US.

Throughout the process, DLocal handles all the “boring but critical” stuff: anti-money laundering (AML) checks, local tax withholdings, and fraud prevention through their Defense Suite.

6.5 How do they make money?

Dlocal makes most of its money by charging fees whenever customers make payments or when businesses send money out. They charge a negotiated fee for each merchant on a per approved transaction basis as either a fixed fee per transaction or fixed percentage per transaction, which varies by solution, applicable geographic market, overall volume processed, and required functionality.

The different types of fees are;

Processing fees

Installment fees

Foreign exchange fees

Other transactional fees

Dlocal also generates revenue from value-added services, such as currency conversion, fraud management, compliance, and risk protection. These services are bundled into the platform, allowing merchants to offload operational complexity and pay extra for advanced features.

6.6 Customers

Dlocal has a wide range of customers as you can see in the picture below. Their focus is on companies that want to broaden their scope internationally, and probably not just one country but a whole range at once.

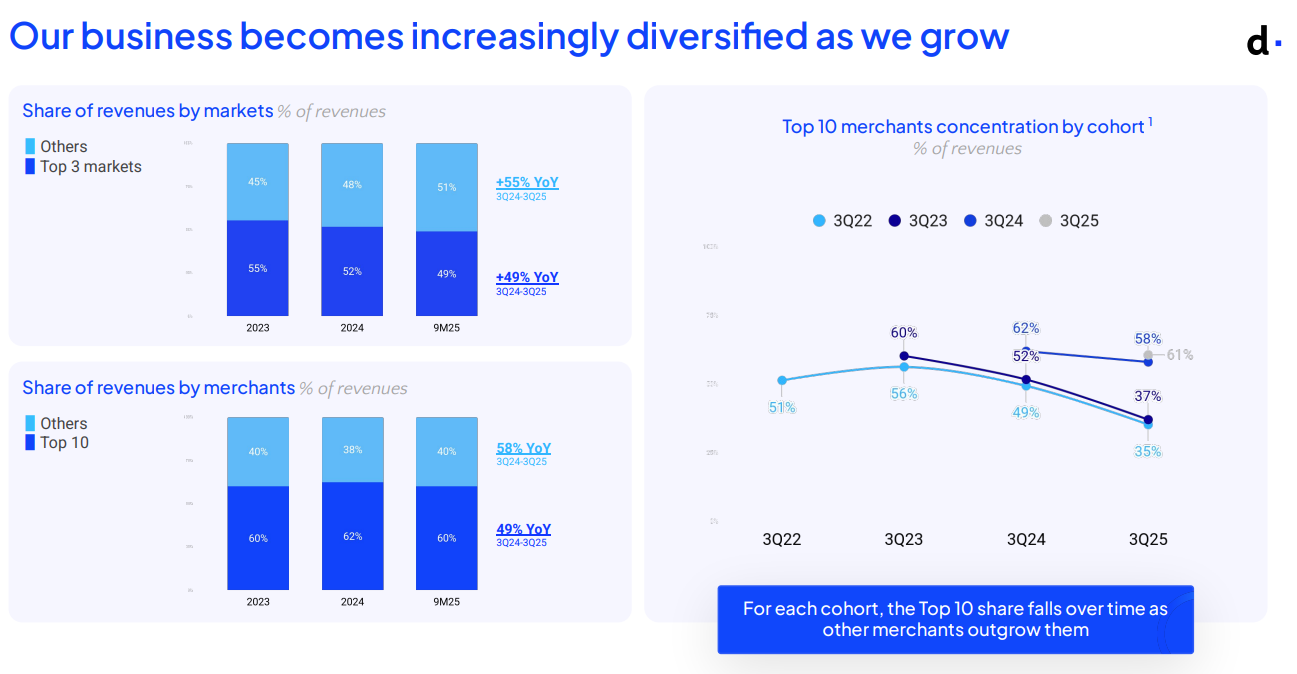

They are quite top-heavy when it comes to client distribution, which has some people worried. The more top-heavy these client are to Dlocal, the more power they have when it comes to negotiating contract-terms. Luckily for us, their is a clear downtrend when it comes to the distribution, and the top 10 share has been falling over time as Dlocal onboards new clients.

7 What is their competitive advantage?

I think the primary competitive advantage they have is their sole focus on Emerging Markets. They are one of the only payment processers that have this specific focus and execute it this well. Does that make them Unique? No. But it makes them specialized. And specialization is what Dlocal’s clients want.