Eli Lilly - Deep Dive

Full Investment Thesis - Eli Lilly

1. Introduction

Some of you might know that I’ve been been a Novo Nordisk shareholder for quite a while now. During that period I’ve done my fair share of research into Eli Lilly, but to be honest, I never really went deep.

To understand the overall GLP-1 landscape, but also to get a good grasp of how Novo Nordisk and Eli Lilly really compete (and sometimes compliment each other), it was time to do a proper research piece on Eli Lilly.

In this deep dive I aim to tell you everything you need to know about Eli Lilly. I will also incorporate my knowledge on Novo Nordisk in this analysis, as I think to fully comprehend Eli Lilly, you have to understand Novo Nordisk as well. That works both ways of course.

I did not do this research to confirm my Novo thesis. If anything, I did it to stress-test it. But, I also wanted to find out if maybe Lilly is the better play. Maybe owning both is the way. We are gonna find out!

So, this is what you can expect in this deep dive:

Full company review; history, management, business model

A look into Lilly’s strength/weakness/risks/opportunities

Deep look into the GLP-1 market + relevant drugs from the main players

Review of Eli Lilly’s financials

Elaborate valuation analysis

My overall approach to benefiting from the GLP-1 rush.

What this is not: a deep dive into all the trial results and in-depth comparison of all the different drugs. I will go reasonably deep on the science because it's load-bearing for the thesis, but this is not a trial deep dive. The overall focus will be on the business side of things.

The core assumptions I want to stress-test in this thesis are the following:

Lilly has the better molecule and is out-executing Novo.

The durable edge is Tirzepatide + Retatrutide, US-manufacturing and (pipeline) diversification.

The key deciding factor for the next decade will be who will win the oral race, in which Lilly is currently behind.”

Now, lets go to it and dive in!

If you want to receive more deep dives like this, make sure to subscribe! Also, if you finish reading it, and thought it was valuable, please give it a like and share it so other people can see it as well!

2. Eli Lilly Origin Story

2.1 How it started

Eli Lilly is the most valuable pharmaceutical company in the world right now. Currently ranking as the 14th largest company, with just over $1T market cap.

Eli Lilly is not a new company, far from it. It was founded in 1876, by who else then the great Colonel Eli Lilly. He was born in 1838 and he was a pharmaceutical chemist by trade.

On May 10, 1876, when he was 38 years old, Eli Lilly opened his own pharmaceutical laboratory in Indianapolis, Indiana. This was not his first try to built a career. After serving in the military at a young age, he tried to get several businesses going, but none of them really succeeded.

But this one did.

Originally, the company began with just three employees, one of them being his own 14-year-old son.

One of the first major innovations and breakthroughs was the gelatin-coating of pills and capsules, which made them easier to swallow. By the end of its first year, the Eli Lilly company had generated a whopping $4,470 in sales. Might sound bad, but that’s actually about $140K in purchasing power today.

Eli Lilly grew steadily in the late 19th century, but the transition from being a regional player to a global player occurred only in 1923. Because that’s when Eli Lilly partnered with researchers from the University of Toronto to mass-produce Iletin, which was the world’s first commercially available insulin.

In the 1940s, Lilly was one of the first companies to develop a method for the mass production of penicillin, which was one of the most frequently used drugs during WWII. The success of penicillin gave them a nice little boost.

The Biotech Era is when things really started moving.

2.2. The Biotech Era

In the late 20th century Lilly moved into the Biotech space, which lead to some of the most famous brand names in the history of medicine. Two names you’ve almost definitely heard heard of:

Humulin: This was “human” insulin, replacing the older animal-sourced versions.

Prozac: Lilly launched Prozac, the first SSRI antidepressant. It revolutionized mental health treatment, became a cultural icon, and was the company’s first “blockbuster” drug which earned them over $1B annually.

They also launched less less famous products like Zyprexa, for schizophrenia and Humalog which is a fast-acting insulin.

2.3. The Diabetes and Obesity Era

The obesity era. This is when the real magic starts to happen. It was the discovery of Tirzepatide that changed everything.

The first Tirzepatide drug that was launch was Mounjaro (in 2022) for type 2 diabetes. Later it was also launched as Zepbound (in 2023), specifically for weight loss/management.

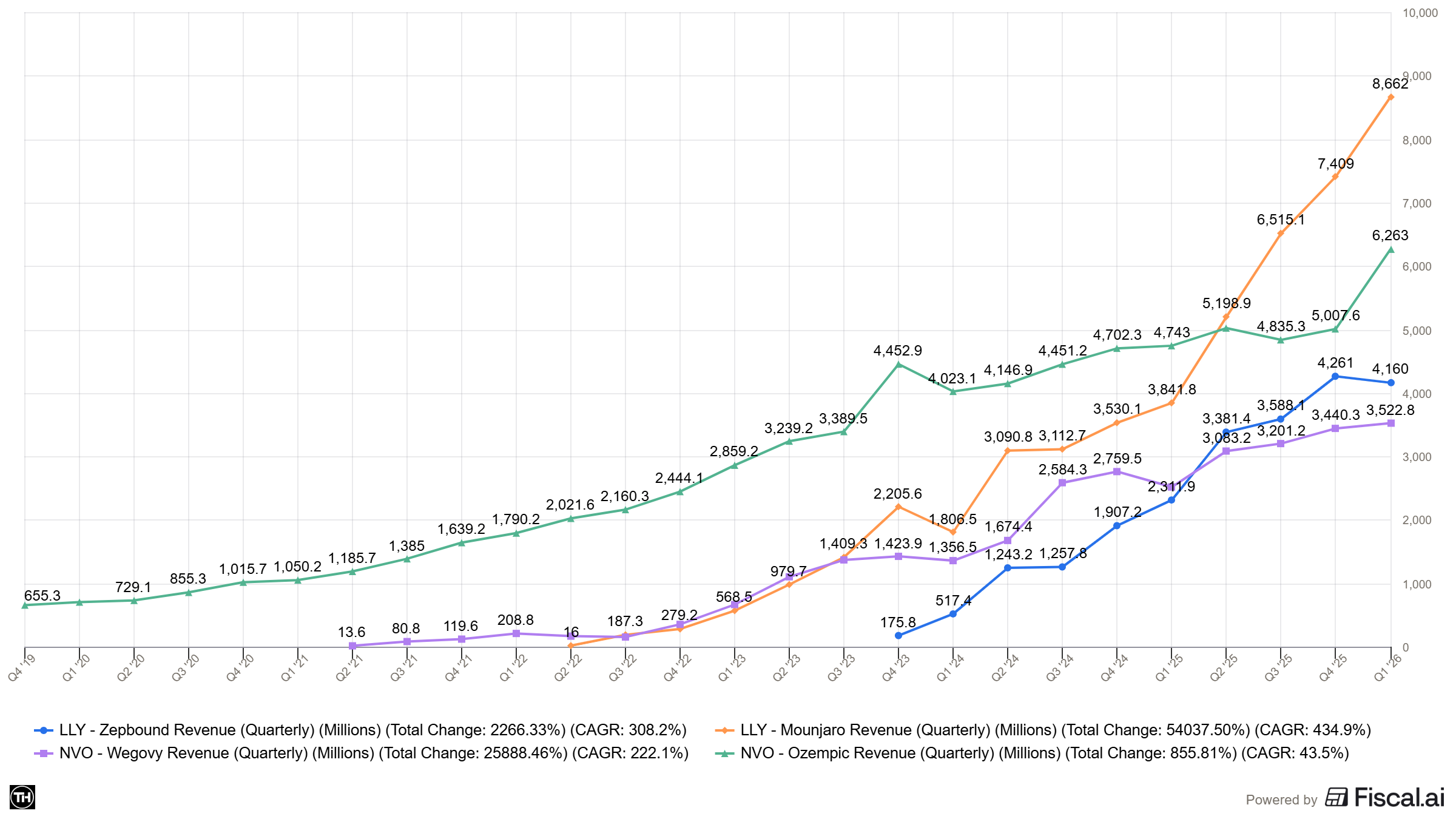

These two drugs were real gamechangers, as they were very strong competitors to Novo Nordisk’s Ozempic and Wegovy. Not just competing, but actually outcompeting. The rise was meteoric, wel’ll see some charts later, and led to over a 400% market cap increase in just the past 5 years.

We will dive into the nitty gritty surrounding the specific drugs and pipeline later in this Deep dive.

But for now all you have to know is: Eli Lilly’s drugs are widely considered to be best-in-class for obesity (and diabetes). Zepbound and Mounjaro are eating Novo’s lunch.

3. Company overview

3.1 Overview

Eli Lilly is headquartered in Indianapolis, Indiana and they currently have around 50,000 employees. Most of these employees are based in North America, about 35,000 of them. The core focus of Eli Lilly is on:

Metabolic diseases (diabetes/obesity)

Oncology

Immunology

Neuroscience (specifically Alzheimer’s)

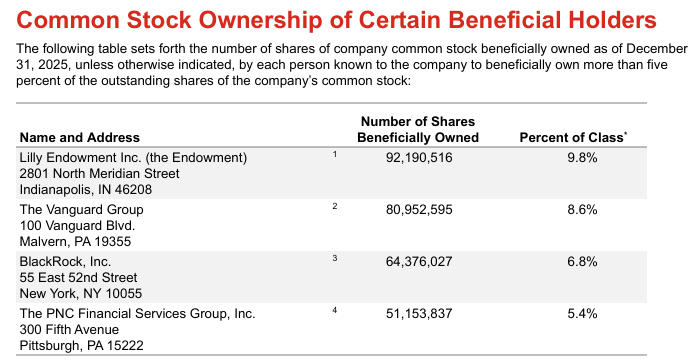

3.2 Ownership structure

Eli Lilly’s ownership structure is quite unique, but that’s mostly because of it’s size. About 80% of shares are held by institutional investors like Vanguard and Blackrock.

Another 10% is owned by the Lilly Endowment fund, which is a charitable foundation created by the Lilly family.

The last part of the puzzle is for retail investors and insiders.

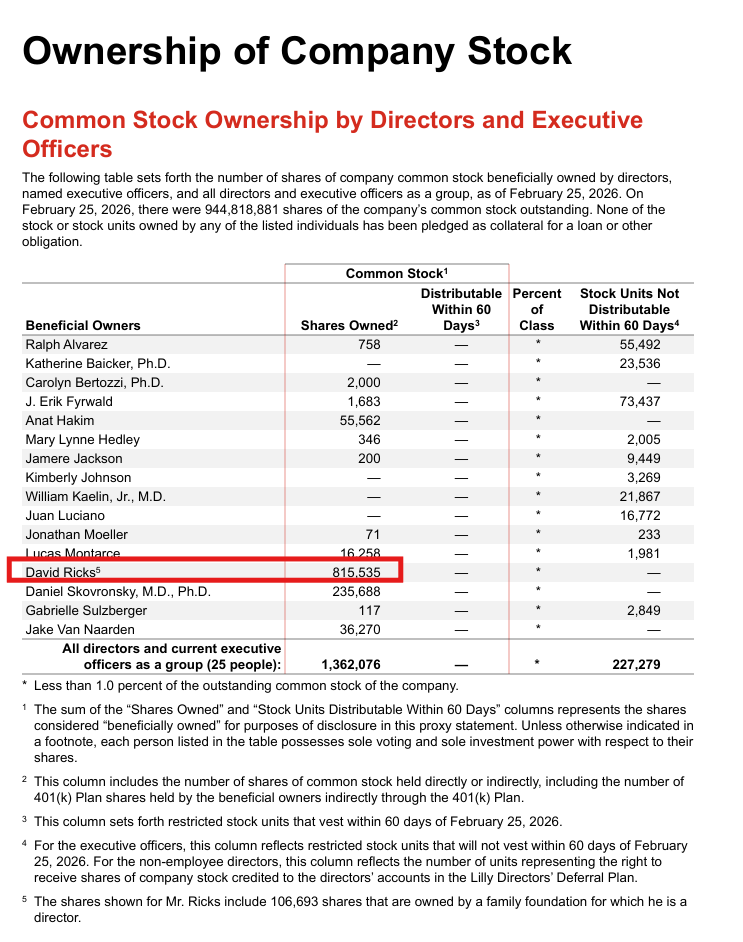

The CEO and chairman David Ricks holds about 815,474k shares, worth close to $917M. This includes 106,693 shares that are owned by a family foundation for which he is a director.

4. Management

A very important aspect for me when looking into a company is the management. As you can imagine, Lilly’s management team is very experienced and all of them have been with the company for quite a while already.

The CEO, David Ricks has been with the company for 30 years now, and most of the management team has been around for at least 20 years.

Lilly historically promotes from within, preferring to create a management team around people drenched in the Lilly DNA, rather than looking for external candidates.

4.1 CEO - David A Ricks

The CEO, Dave Ricks, has been with Lilly for a long time, now closing in on 30 years with the company. David became CEO in January 2017 and was elected chair of the company’s board of directors effective June 2017. Before that he worked in marketing, sales, drug development and international operations.

He had made name for himself when he led Lilly’s growth in China and Canada. I would argue he is not afraid to take risks. He doesn’t shy away from making big decisions and really shifting into next gear when he sees an opportunity. He’s proven that multiple times throughout his career.

He famously pushed to cut drug development timelines in half, especially during the scale-up of Mounjaro and Zepbound. That was really big for the sector, but also for the speed at which Lilly was able to rise as fast as they did.

If you want to get a good feel for David as a person, and how he approaches running and building a business, I’d highly recommend the podcast below. It’s a quite open and transparent interview.

David Ricks - In good Company Podcast

I noticed he’s a CEO that’s quite heavily invested in creating a specific type of corporate culture.

The first thing he often mentions is that he wasn’t to spark and encourage curiosity.

Secondly, he wants to create a sort of family-like culture. I know that’s something that a lot of companies want to achieve, but the way he describes it resonates with me.

The overall culture seems very cordial and respectful. He even mentions people call it ‘‘Lilly Nice’’.

He also mentioned during other interviews that he prefers a culture of debate, a place where everyone in the leadership-team has an equal voice. Of course there will always be hierarchy, but he truly believes in learning from bottom-up as well.

He is not afraid to make public appearances, as he frequently does public interviews and podcasts. Nothing wrong with that in my opinion. It’s a nice way to gain some visibility and credibility.

4.2. CFO - Lucas Montarce

Lucas Montarce spent over two decades rotating through nearly every critical financial and operational sector of the business before becoming CFO.

He served as the CFO of Lilly International and most recently as the President and General Manager for the Spain, Portugal, and Greece hub. He was the CFO of Lilly Research Laboratories (LRL), where he worked closely with the scientific teams to align financial resources with drug discovery.

4.3 Chief Scientific & Product Officer - Daniel Skovronsky

Dr. Skovronsky joined in 2010 when Lilly acquired his startup, Avid Radiopharmaceuticals. He rose quickly, becoming Chief Scientific Officer in 2018. As of late 2025, his role was expanded to oversee not just R&D, but the entire global product strategy for metabolic, immunology, and neuroscience

4.4. (EVP & President, Lilly International) -Patrik Jonsson

Jonsson joined as a sales representative in 1990 in Sweden. Over 35 years, he has led nearly every major geographic hub, including Italy, Japan, and the United States, before taking over the entire International division in 2025

5. Obesity/Diabetes Market and TAM

Before we start, let’s make it clear that obesity and diabetes are getting very intertwined. Diabetes was sort of like the foundation, and that infrastructure is now being used to dominate the obesity market.

Both business models are designed to treat the entire spectrum of metabolic health, even allowing a patient to move from diabetes management to weight loss and other related areas like heart and kidney health.

What Lilly and Novo both do: sell the exact same chemical compound under two different names, one for diabetes and one for obesity.

This allows them to navigate different insurance coverage rules and marketing regulations.

More on that later

5.1 Obesity

Let’s define what Obesity actually is:

Obesity is a complex, chronic disease defined by excessive, abnormal body fat accumulation that poses significant health risks. It is generally diagnosed in adults with a Body Mass Index (BMI) of 30 or higher.

There are usually 3 classes in obesity:

Class I (Obese): BMI 30.0–34.9

Class II (Moderate): BMI 35.0–39.9

Class III (Severe/Morbid): BMI 40.0 or higher

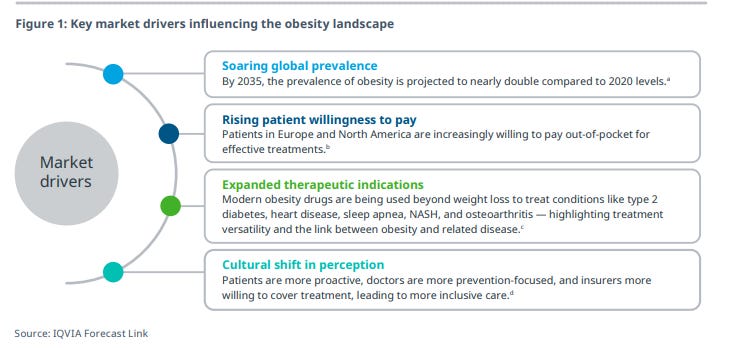

We all know obesity is a big thing, punt intended. Some even talk about a pandemic.

That’s because bbesity numbers are rising fast, mostly in first-world countries. But in the last decade there’s also a sharp uptick in EM-countries like in Brasil and China.

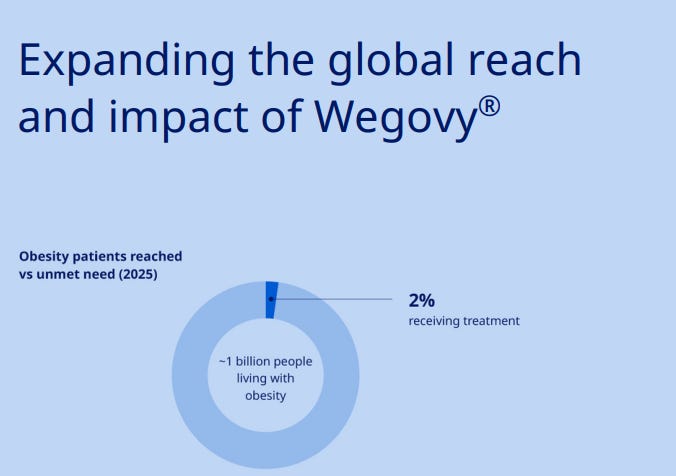

According to Novo Nordisk, who openly share there research on this matter, there are currently 1 billion people living with obesity and/or diabetes in the world. Of those 1 billion people, only 2% is currently receiving treatment. The addressable TAM is there for taking.

Obesity can be found in most parts of the world, but Europe, North America and South America are definitely the key focus areas for both Lilly and Novo Nordisk. It's estimated that two in five adults in the United States live with Obesity.

As you can see in the picture below, these aeras have the highest numbers of obesity in the world. There are also parts in Africa and the Middle east with high obesity numbers, but they do not get the same attention, yet.

This is likely because of the unorganized healthcare systems and these usually ‘‘poor’’ aeras simply cannot afford medication.

")

IQVIA (which is a global leader in healthcare information) estimates that by 2035, 1.53 billion adults will be suffering from obesity. Keep in mind, this does NOT include the overweight segment. If you include overweight people as well, the total number would reach 3.3 billion people (over half of the world population).

The financial impact is equally significant, with these conditions projected to reduce the global economy by more than $4T annually by 2035, equivalent to nearly 3% of global GDP.

IQVIA projects that between 2026 and 2034, the global AOM (anti obesity medication) market is expected to grow at a CAGR of 13–15% and the total market size is expected to reach approximately $130B.

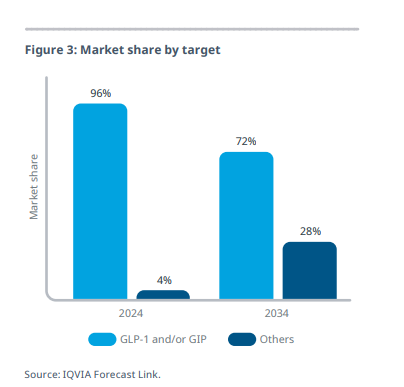

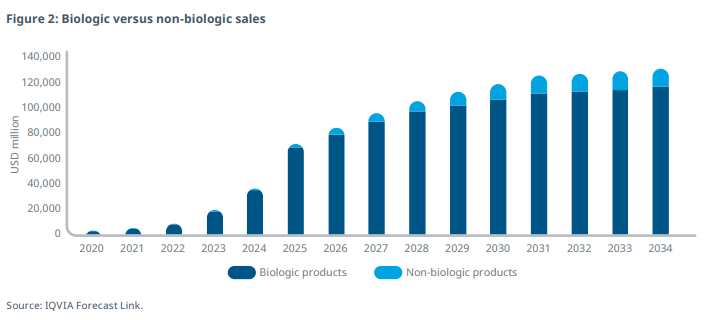

Biologics are leading the way in the obesity drug market, with GLP-1 and GIP receptor agonists holding the major share.

However, non-biologics are expected to regain some market share in the forecast period as the market diversifies and new treatment options emerge.

5.2 Diabetes

What is Diabetes?

Diabetes is a chronic metabolic disease characterized by high blood sugar (glucose) levels, resulting from the pancreas producing insufficient insulin or the body inefficiently using it. It causes serious, long-term damage to nerves, blood vessels, eyes, kidneys, and the heart.

Lilly and Novo both used to be ‘‘diabetes companies’’. They focused on both type 1 and 2 diabetes, and it’s important to know the difference.

Type 1: An autoimmune condition where the pancreas produces little to no insulin.

Type 2: The body does not use insulin effectively (insulin resistance) and cannot produce enough to compensate.

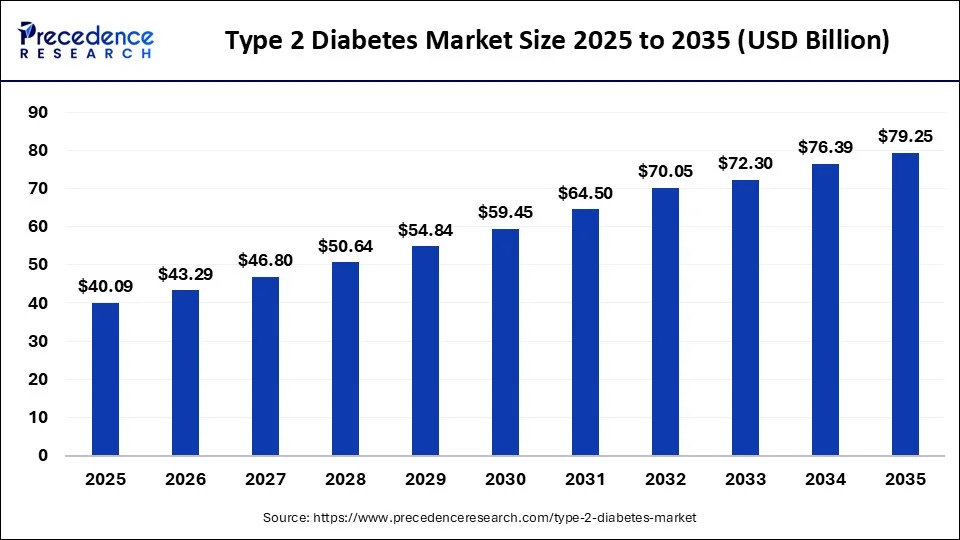

For diabetes, a similar marco-trend is witnessed as is with obesity. According to Precedence Research, the global type 2 diabetes market size is predicted to reach around $79.25B by 2035, increasing from $43.26B in 2026, expanding at a ‘‘healthy’’ (yes pun intended again) CAGR of 7.05% from 2026 to 2035.

That’s significantly slower than the obesity sector, but still decent growth. As you can imagine, the focus for both Lilly and Novo is on the obesity sector right now. And that makes perfect sense.

Growth is supported by better screening and early diagnosis, along with the rising use of advanced treatments like GLP-1 therapies for blood sugar control and weight management. Improving healthcare access is also helping expand treatment adoption.

The global type 1 diabetes market size is calculated at $37.60 billion in 2025 and is predicted to increase from $40.54Bin 2026 to approximately $79.14B by 2035, expanding at a CAGR of 7.73% between 2026 and 2035.

5.3. GLP-1 Market

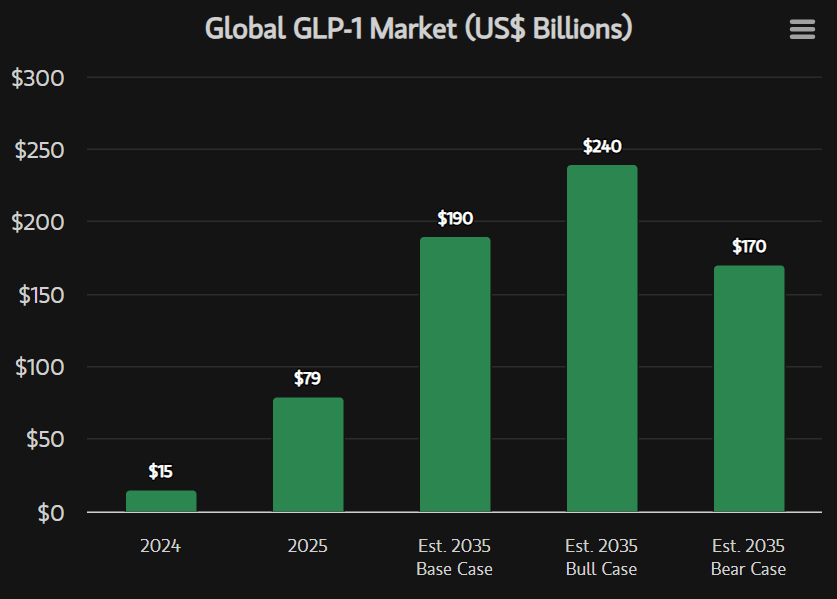

Looking at the total GLP-1 landscape, steady growth is expected in the next decade. Morgan Stanley estimates that the GLP-1market can scale from just shy of $80B in 2025 to $190B in 2035.

They state that the GLP-1 market is at an inflection point, mostly because of the launch of oral therapies and the expansion of Medicare access in the U.S.

This new wave of potential clients should do well for overall adoption.

In Morgan Stanley’s base-case scenario, nearly 30% of the obese or diabetic population in the U.S. and 10% in the rest of the world are likely to be treated with GLP-1 therapies by 2035, up from approximately 6% in the U.S. and 2% internationally in 2025.

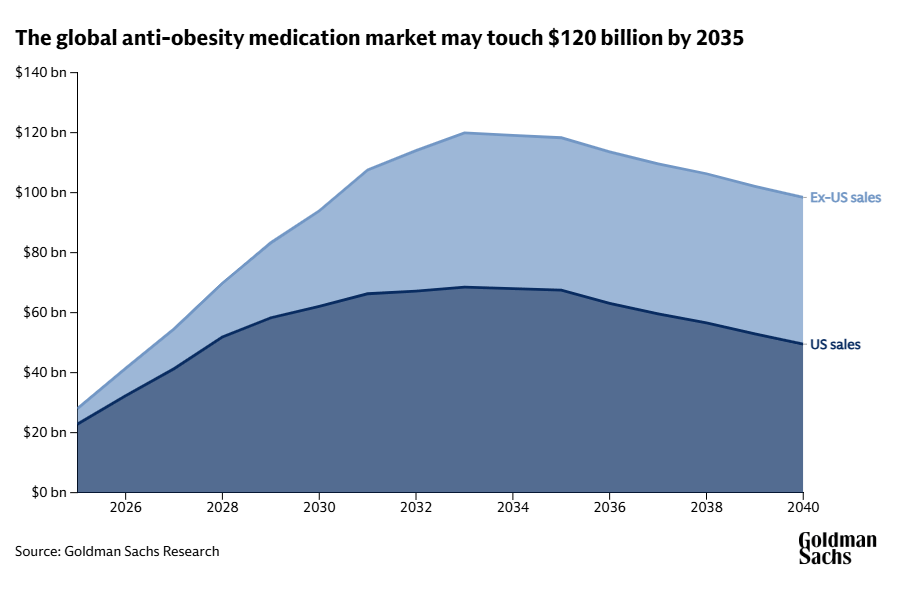

I also looked at the forecasts from Goldman Sachs, who are certainly not as bullish.

Goldman Sachs Research forecasts the global market to reach $95B by 2030, which is lower than its previous estimate of $130B. This new figure reflects trends influencing how these drugs are priced, how long patients stay on them, and how patient populations are segmented

They do however see a lot of room for growth in non-US markets, which is clearly visible in their outlook below.

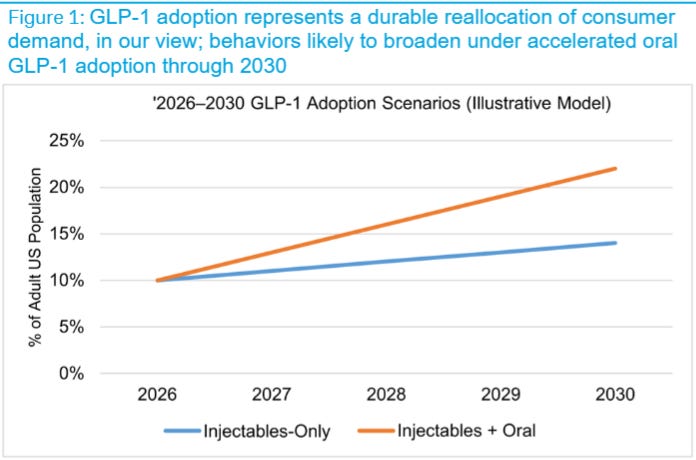

Then we have Deutsche bank, they too expect GLP-1 adoption to significantly increase in the next few years, especially the combination of oral + injectables. Demand is certainly there. And yes, why wouldn’t it be with the obesity numbers increasing so much?

I’m somewhere stuck in the middle of it all. I think the GLP-1 market will definitely continue growing, but it will all depend on availability, price and worldwide adoption.

It’s hard to put a number on it. Especially with the the oral market just opening up. The long-term impact, but also the long-term effects on how many new patients will come to the market is difficult to assess.

But the simple fact is. This market will grow. It will grow fast. But how fast, is just open to interpretation.

I’d like to quote IQVIA here, as this perfectly reflects my reasoning:

By the end of the decade, the obesity market enters a far more competitive and mature phase.

It is no longer useful to think of obesity as a single, monolithic market. Instead, the market becomes highly complex and deeply segmented, shaped by body mass index, comorbidities, and by differences in patient profiles and preferences, including route of administration, dosing frequency and tolerability.

6. Eli Lilly Product offering

6.1 Segments

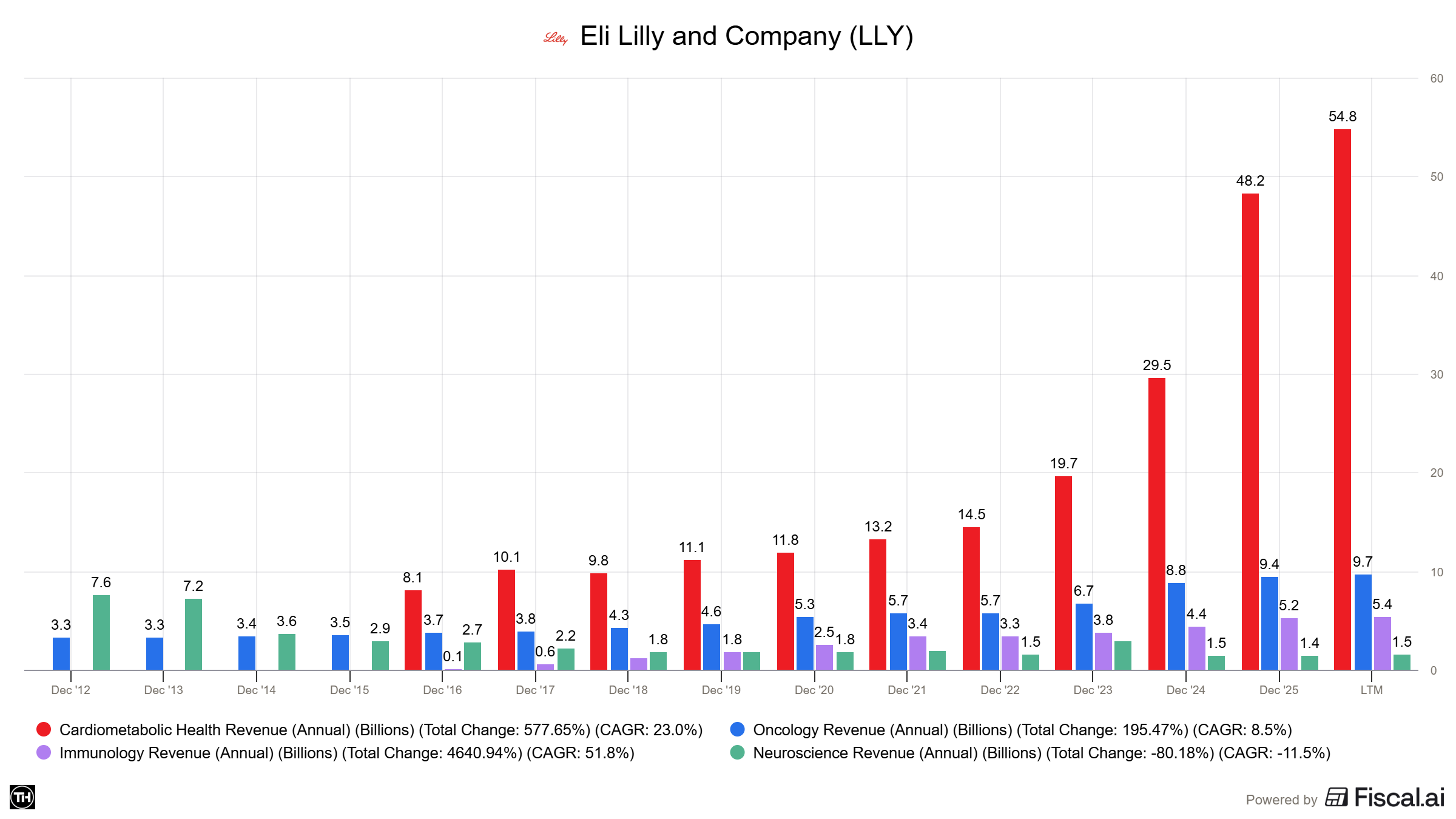

In my opinion, Eli Lilly has a more diversified portfolio right now than Novo Nordisk. The majority of their revenue comes from the segment they call Cardiometabolic Health (CH), this includes diabetes and obesity). The segment makes up 76.7% of total revenue and it’s share is increasing. The other segments make up:

Oncology: 13.6%

Immunology: 7.6%

Neuroscience: 2.10%

As you can clearly see below, CH is also by far the fast growing segment. This is the primary focus for now and the future for Lilly.

6.2 Key contributors

So which drugs are the main contributors to overall growth?

Right now, It’s Mounjaro and Zepbound. And it’s not even close.

I’ll tell you more about them later, but first we have to understand what Tirzepatide is and why it’s so competitive. Because this molecule is actually the core of Eli Lilly’s success.

6.2.1 Tirzepatide

Tirzepatide is the active ingredient in both Mounjaro and Zepbound. It’s a so-called Dual Agonist.

That means that it basically mimics two hormones (GIP and GLP-1). The are hormones that regulate appetite, feeling satisfied and blood sugar.

GLP-1 controls hunger and blood sugar and GIP is thought to improve how the body breaks down sugar and fat.

For comparison, Semaglutide (which is Novo’s active ingredient for Ozempic and Wegovy) only targets the GLP-1 receptor.

In head-to-head trials, Tirzepatide showed greater, faster weight reduction than Semaglutide, and that’s one of the key reasons why it’s so popular.

Mounjaro, Wegovy, Ozempic and Zepbound are given once per week as injections under the skin (subcutaneously) in the stomach area, thigh or upper arm.

Both Lilly and Novo have also been working on an oral version. Novo has started sales of their Wegovy pill in January of this, and Foundayo (basic ingredient is Orforglipron), which is Lilly’s counterpart), came to market in April..

More on the oral versions and how they are doing later.

6.2.2. Mounjaro + Zepbound

Mounjaro came to market first. It is FDA-approved to treat Type 2 Diabetes and it is a once-weekly injection. It is intended to help people with diabetes lower their A1C (average blood sugar) and improve insulin sensitivity.

Lilly ran five main studies (SURPASS-1 through 5) to see how Tirzepatide stacked up against existing treatments. Even though these were diabetes trials, people lost between 8% and 14% of their weight, which tipped Lilly off that they had a massive weight-loss drug on their hands

In general: the higher the dose, the higher the weight loss.

A few years later, Zepbound was brought to market, specifically targeting weight loss management.

It is approved for adults with obesity (BMI 30+) or those who are overweight (BMI 27+) with at least one health issue like high blood pressure. In late 2025, it was also approved to treat Obstructive Sleep Apnea.

Side effects

Like with most of the weight-loss drugs, both have positive and negative side effects. Some of the positive ones are:

Significant reduction in the risk of heart attacks and strokes

It helps clear fat from the liver (MASH) and reduces strain on the kidneys

It combats chronic joint pain or general "puffiness" seems to disappear, likely due to anti-inflammatory effects

The negative ones are quite common and well-known:

Nausea, diarrhea, and constipation are very common (about 20-30% of users)

Smelly breath, often compared to the smell of eggs

Very rare: risks of pancreatitis, gallbladder issues and a rare type of thyroid tumor (not seen with humans yet, only in rats)

And a side-effect that’s related to almost every comparable drug: the loss of muscle mass. If you lose weight too fast without eating enough protein or lifting weights, you can loses muscle mass along with the ‘‘regular’’ fat.

Mounjaro and Zepbound have taken the market by storm. Eating away the early mover advantage Novo Nordisk had with Ozempic and Wegovy.

Simply put: the Tirzepatide drugs are widely regarded to be the ‘‘better ones’’, compared to the Semaglutide counterparts.

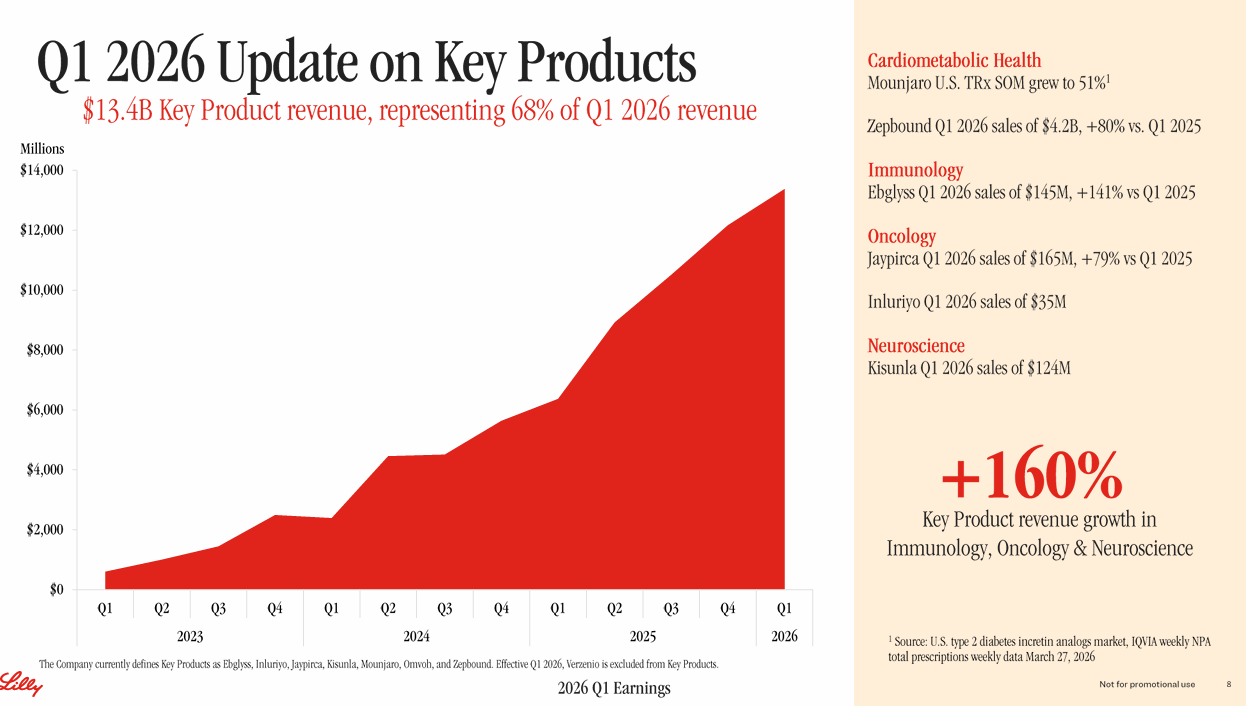

While Mounjaro and Zepbound are running the show right now (bringing in $36.5 billion combined in 2025), Eli Lilly has some other relevant drugs to mention as well.

Here are the drugs contributing the most to Lilly’s revenue after the big two.

I will talk about Foundayo later, as this was has just been released and numbers are unclear.

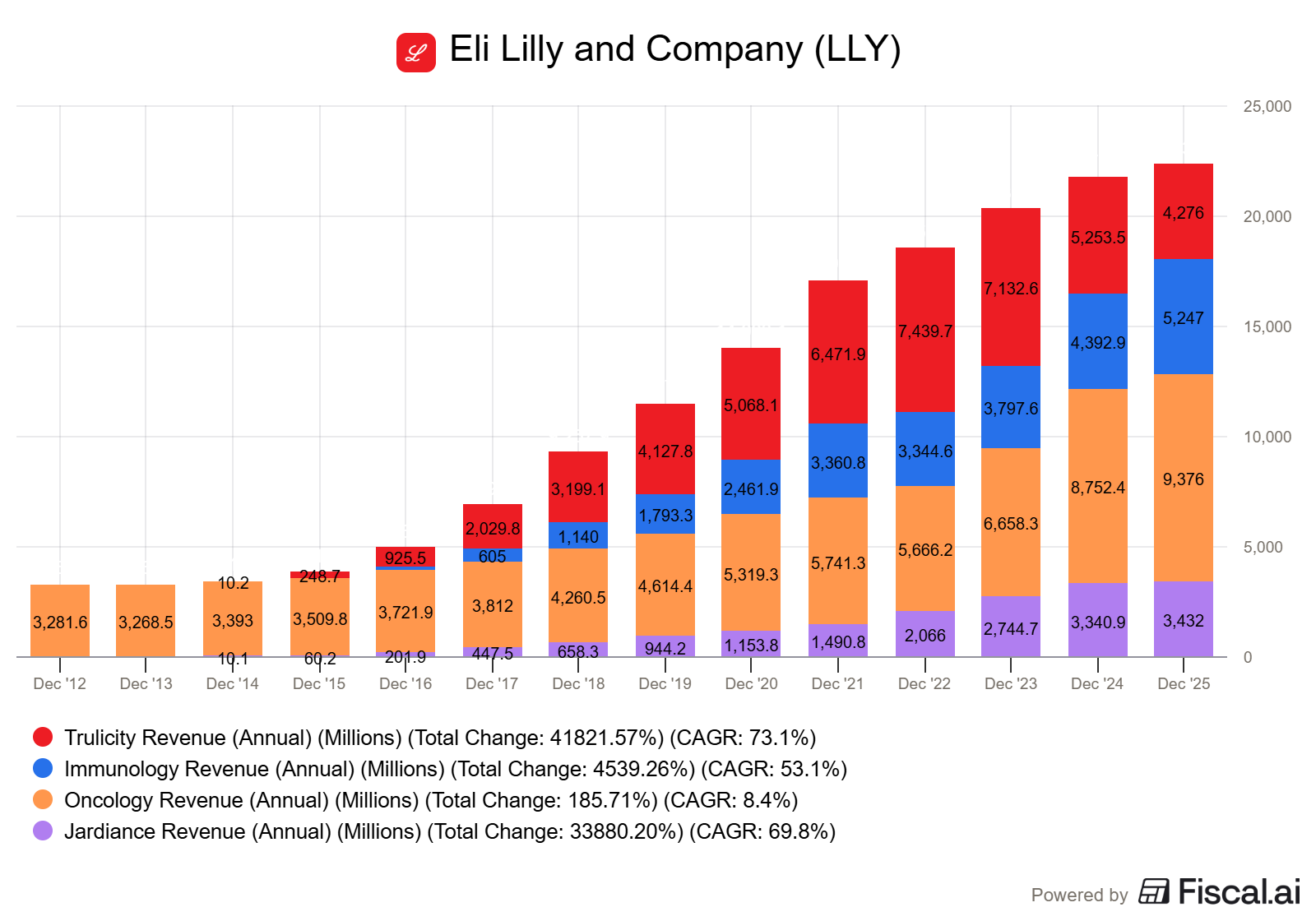

1. Verzenio (Cancer)

This is Lilly’s clear number three. In 2025, it pulled in $5.72B. It’s used to treat certain types of breast cancer, and while its growth isn’t quite at “weight-loss drug” speeds, it’s a massive, reliable revenue engine that continues to expand into earlier stages of treatment.

2. Trulicity (Diabetes)

Trulicity is in a bit of a “graceful retirement” phase. Because it’s an older GLP-1, many patients are switching over to Mounjaro. Even so, it remains a multibillion-dollar product, likely landing in the $4–5B range for 2025 despite double-digit declines.

3. Jardiance (Diabetes & Heart Failure)

Jardiance contributes around $3.5B annually. It has stayed relevant by proving it’s good for more than just blood sugar and it’s also widely prescribed for heart failure and chronic kidney disease.

4. Taltz (Immunology)

For plaque psoriasis and psoriatic arthritis, Taltz is Lilly’s go-to. It consistently generates over $3B a year. It’s a competitive market (fighting against giants like AbbVie’s Humira/Skyrizi), but Taltz has carved out a very profitable niche.

Some other noteworthy ones are, Inluriyo (both oncology) and Kisunla which is their Alzheimer bet.

6.2.3. Foundayo

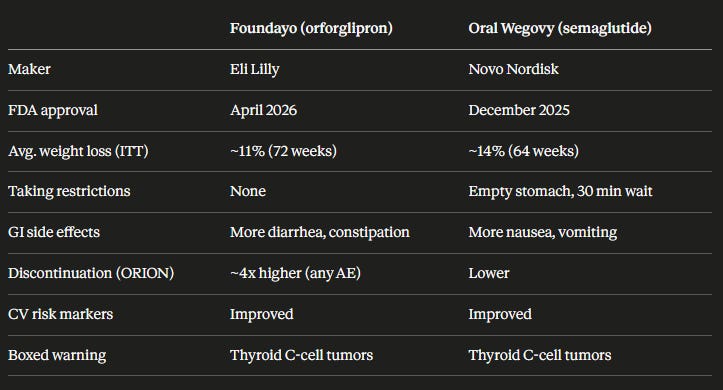

Now, let’s look into Foundayo for a bit. Because in my opinion what happens in the oral space, will determine the next winner.

Foundayo is Eli Lilly’s bet in this segment.

Foundayo (with the core ingredient Orforglipron) is a once-daily small molecule (non-peptide) oral GLP-1 receptor agonist,

The "small molecule" is actually important to keep in mind, because unlike Semaglutide, which is a peptide drug requiring strict handling conditions, Orforglipron is a small molecule, meaning it follows standard small-molecule chemistry and doesn't require the same formulation complexity as peptide-based GLP-

Foundayo was FDA approved on April 1st, really no joke. It was available in markets soon after.

Looking purely at weightloss, the Wegovy pill is ahead.

In the ATTAIN-1 trial, people taking the highest dose who stayed on treatment lost an average of 12.4%, compared to 0.9% for placebo. Including everyone who started the trial, not just completers, the average was 11.1%.

Oral Wegovy’s numbers are higher. In the OASIS 4 trial, oral Semaglutide 25 mg achieved 16.6% mean weight loss at 64 weeks with full adherence, compared to 2.7% for placebo. One-third of adherent participants achieved at least 20% weight loss. Including dropouts, the average was 13.6%.

Foundayo 12.4% vs oral Wegovy 16.6% (efficacy estimand)

Foundayo 11.2% vs oral Wegovy 13.6% (Both all-comers:)

So that means 11.2% for Foundayo and 13.6% for Wegovy, which is a significant win for Wegovy.

Where Foundayo genuinely wins is usability. Foundayo can be taken any time of day without food or water restrictions, whereas oral Wegovy must be taken in the morning on an empty stomach with no more than four ounces of water, waiting 30 minutes before eating or drinking.

Personally I think this usability benefit is really overstated.

Here are the differences summarized.

Some new data came in on June 8:

Lilly reported Foundayo beat oral semaglutide head-to-head in type 2 diabetes (ACHIEVE-3): 9.2% weight loss and 2.2% A1C reduction at 17.2 mg vs 5.3% / 1.4% for oral sema. Lilly plans to file Foundayo for T2D with the FDA by end of Q2.

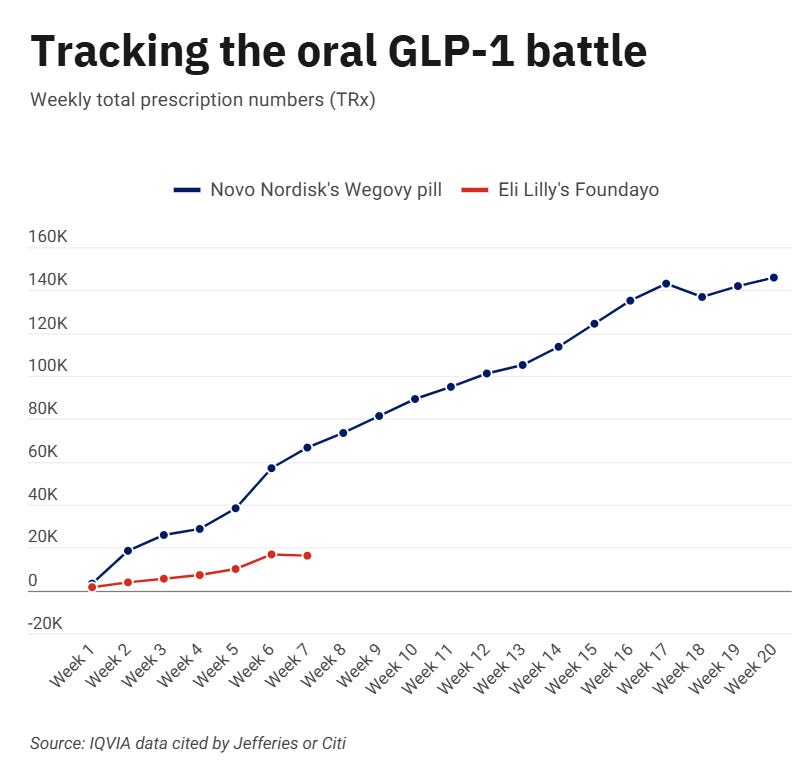

Foundayo’s launch

Foundayo’s launch has been a bit underwhelming to say the least. Compared to the Wegovy pill launch, Foundayo is clearly underperforming.

Lilly stated that this is due to their need to build brand awareness. CVS Caremark removes the new-to-market block on Foundayo effective June 1, 2026.

Foundayo’s performance still tracks ahead of Novo’s injectable Wegovy and Lilly’s Zepbound at the same point in their respective rollouts, so it might look worse on a first glance that it actually is.

Eli Lilly stated multiple times that they believe their targets can still be met. Analysts believe that Foundayo will rack in about $145M in the Q2, and even reach $1.6B for the full year. (source Jefferies)

6.2.4. Eli Lilly’s Pipeline

Now, lets briefly discuss Eli Lilly’s pipeline, because there is one very important drug that is high anticipated. Retatrutide.

This is Lilly's next-generation obesity drug, and the data looks very promising. Mounjaro/Zepbound hit two receptors (GIP + GLP-1), but Retatrutide is a triple hormone receptor agonist that activates GIP, GLP-1 AND glucagon receptors.

Weightloss numbers look very strong. In the TRIUMPH-1 trial, participants on 12 mg Retatrutide lost an average of 28.3% of body weight over 80 weeks. 45.3% of participants achieved ≥30% weight loss.

Lilly is studying Retatrutide across multiple Phase 3 trials, focusing on obesity, type 2 diabetes, knee osteoarthritis, sleep apnea, chronic low back pain, cardiovascular and renal outcomes, and metabolic liver disease.

FDA submission is likely coming in 2026/2027 if the remaining readouts hold up

Some other noteworthy drugs in the pipeline:

Tirzepatide: The base drug is already approved for diabetes and obesity, but Lilly keeps expanding its label

Kisunla (donanemab) for Alzheimer's

Eloralintide: amylin receptor agonist heading to phase 3, at ADA it showed 20% weight loss on the amylin pathway alone

MORF-057: bit of a wild card, after the $3.2 billion acquisition of Morphic. This is a oral integrin inhibitor targeting ulcerative colitis and Crohn's disease, currently in Phase 2

Main focus is and will be on Tirzepatide, which is expected to further bolster Eli Lilly’s strong position in the GLP-1 market.

6.5. Noteworthy pipeline developments for Novo Nordisk:

A quick sidenote, because last weekend Novo presented a lot of new data. I didn’t get a chance to dive in deep, but there where some noteworthy headlines to take into consideration. I’ll mention them here, as they do provide more insight into Novo’s pipeline.

CagriSema (REIMAGINE, type 2 diabetes) Three Phase 3 trials published at ADA in The Lancet. REIMAGINE-2 (the metformin arm) is showing ~1.91% A1C and ~14.2% weight loss over 68 weeks.

Zenagamtide (formerly amycretin) Single-molecule GLP-1/amylin agonist. Phase 2 in T2D: up to 14.6% weight loss and 1.71% A1C at 40 mg / 36 weeks. That looks strong, but ~34% of patients on the 20/40 mg doses withdrew (at 40 mg: 37% nausea, 29% vomiting, 37% diarrhea). Phase 3 starts H2 2026, first results are not expected before 2028.

UBT251 is Novo’s triple agonist, acquired from United Laboratories (China) in 2025. It showed~19.7% at 24 weeks at the top dose with no plateau yet. Caveat are the demographics: heavily female (~60–64%), young (~33 yrs), and lower starting BMI (~33 vs ~37 for Retatrutide’s Phase 2).

These are the most noteworthy competitors for Lilly in the future, so we should keep tracking them.

I will be doing a GLP-1 deep dive later this year, and I will cover the trial-data more in-depth then.

This is the end of the free part of the Deep Dive. The next part is for paid subscribers only.

Paid subscribers get access to: all my buys/sells, all of my portfolio updates, access to the private section of my discord, exclusive content, my investment library and my full access to all deep dives and articles.

In the last section I cover:

Lilly’s business model

Lilly’s competitive advantage

Lilly’s competitors and how they stack up

Risks and headwinds

Deep dive into the financials

My bear/base and bull case valuation models

My plan and approach for Eli Lilly and the GLP-1 sector