STIF (ALSTI) Valuation Model update

STIF (ALSTI) Valuation Model update + Short recap of 2025 earnings.

Good day to you all

STIF dropped about about 20% after releasing 2025 numbers yesterday.

In this article I will give you my updated valuation models plus I will tell you what I’m doing with the position.

If you haven’t yet, I would highly recommend checking out my investment thesis here:

Even though in my opinion not much new was added in the 2025 report that was published yesterday there were some broader concerns I’d like to highlight.

Top-line growth was still strong 47.8%, but profitability is taking a hit. The gross margin dropped from 64.7% in 2024 to 63.0% in 2025.

Also, the EBITDA margin shrank from 25.6% down to 22.7%. Starting to fall in line already with management’s 2030 targets.

Net profit came in at €11.8M, but the market had higher expectations. So I believe that is the main reason for the drawdown. A big hit on profitability is not something the market likes to see.

STIF bought revenue growth through the STUVEX and BOSS PRODUCTS acquisitions.

Management explicitly stated that these new acquisitions have operating profitability levels below the Group’s historical standards.

Funding these acquisitions pushed net debt to €24.3m. Because of this, their financial expenses went from €0.2M in 2024 to a €1.8M drag on earnings in 2025.

Management reaffirmed long-term goal of €200M by 2030 and EBITDA margins of 20%.

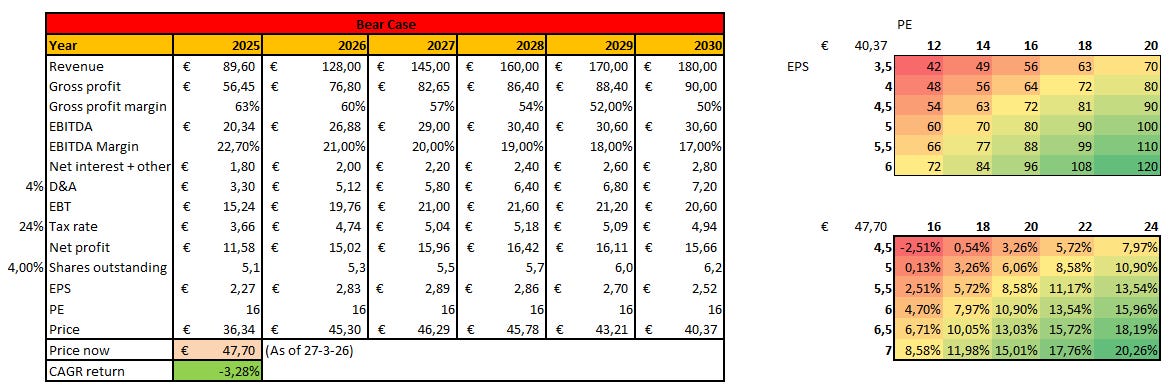

So, let’s use all the new information we have into the valuation models. I will give you my bear/base/bull case and end with a weighted average CAGR.

In the bear case, with very conservative assumptions we get a -3.28% CAGR