Constellation Software - Deep Dive

Full investment Thesis - Constellation Software

1. Introduction

Welcome to my second deep dive of the year! I’ve had a lot of fun researching and writing about Constellation Software.

Constellation Software is interesting on so many levels: the way it was built from the ground up, its unique structure, the way employees have skin in the game, the diversification story, and let’s not forget: its performance over the last few decades. Since 2010, the share price has risen a whopping 6,500%.

There are many lessons to be learned from Constellation’s story; not just about running a business, but also about company culture, establishing principle-based guidelines, and focusing on core competencies. Mark Leonard is easily one of the most inspiring and unique CEOs of the past few decades, and what he has built will likely remain unparalleled for years to come.

I aim to cover all of that in this deep dive. Please keep in mind that I am not a financial advisor, nor am I an expert in this particular field. This is simply me sharing my research with all of you.

I hope you learn a thing or two and enjoy the read. Now, let’s dive in!

Please like and share or comment this post if you thought it was valuable. It helps me out tremendously and ensures that as many people as possible see my work.

2. Why does the opportunity exist?

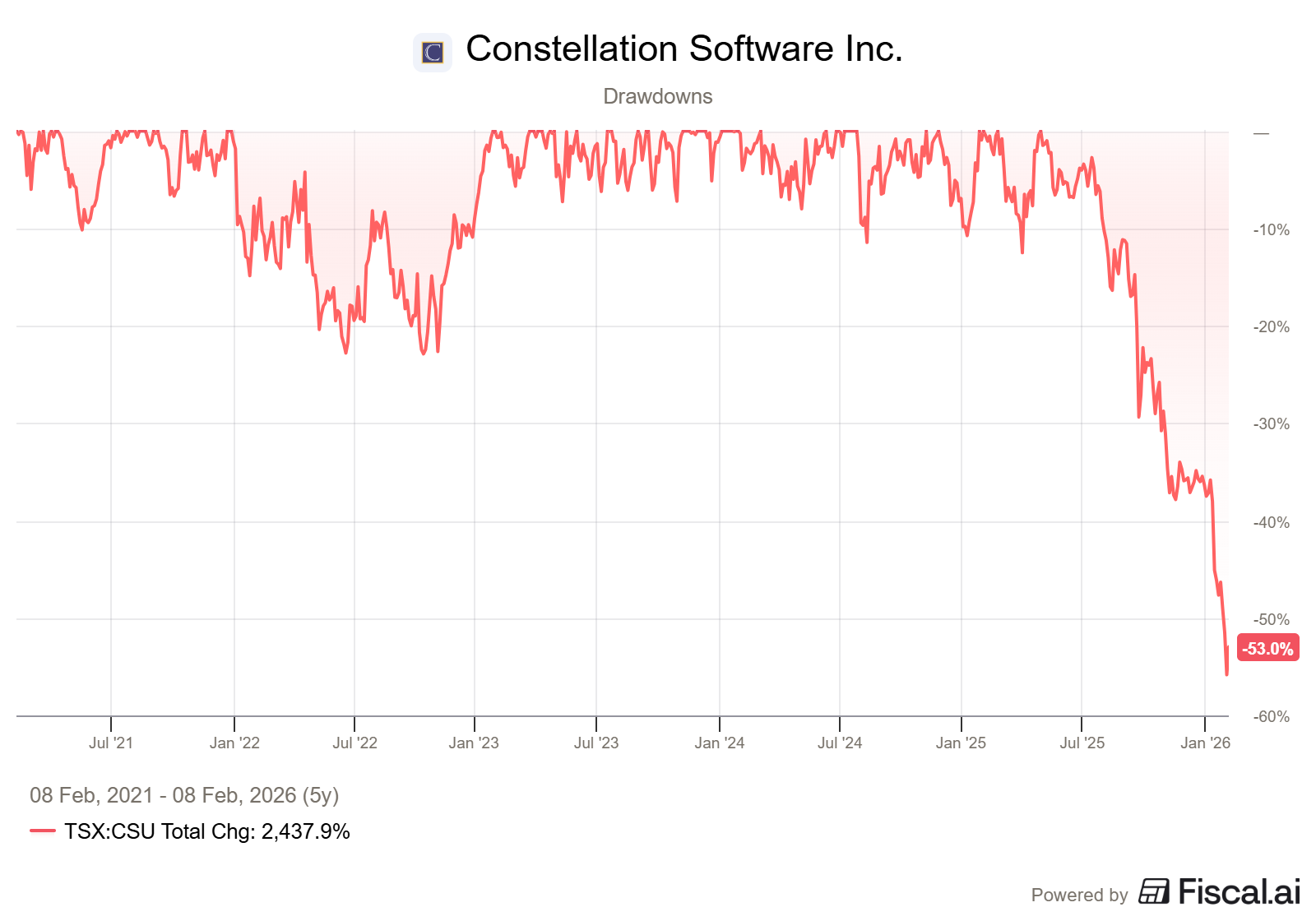

2.1 The drawdown

Constellation Software (CSU) is a company that I’ve been following for a while now, but I’ve never pulled the trigger. My main concern was: the ‘‘steep valuation’’. Stupid in hindsight, because such a high quality company deserves a steep valuation. But now, over the past months, something unique has happened.

As of couple months ago, CSU’s stock price is in free fall. The share price has fallen more than 50% from it’s all-time high. Unprecedented for CSU.

Before this drawdown, they had never experienced a drawdown bigger than 20%, so this is very unique and it warranted more research in my opinion.

So I was curious, why on earth is the stock falling like this? I found three major reasons:

Mark Leonard stepping down as CEO due to health reasons

Uncertainty of the impact of AI (tools) on Constellation’s businesses

Worries that the addressable TAM might be limited (the amount of companies that can be acquired in the VMS-sector)

I’m going to address address all three of them first, before we look into CSU deeper. This will already give you a good insight in what is going on, before we explore the the other parts of the company

2.2 Mark Leonard (CEO) Stepping Down

So, shares falling on this news I can completely understand, not saying it’s fair, but it’s reasonable. Mark Leonard was (and still is to this day), the visionary behind CSU’s success. He built the company from the ground, applied his values, applied his standards, and made CSU to what it is today. If the grounding father leaves a company, that hurts.

But in my opinion it does not warrant a sell-off like we’ve seen these past months. What Mark Leonard has been working on for the past decade, is making sure the company does not resolve around one single person. The business is multi-layered with different operating units and subsidiaries. There are many different smart people that run these units individually, and to this day, with great success.

After Mark Leonard stepped down in september, he was replaced by Mark Miller. With Mark Miller, they seemed to have found a worthy replacement. He has been with Constellation Software for decades and led major units like Volaris, and has deep experience executing the same decentralized, buy-and-hold approach. Note-worthy: Volaris was one of the best performing units of CSU when Mark Miller was running the show. They actually had a slightly different approach than other segments and the parent company.

Instead of sending FCF back to the parent company, Volaris reinvests it’s FCF almost immediately into new, smaller acquisitions within its own "ecosystem." Volaris uses its own FCF to fund its growth, effectively acting as an autonomous “compounder” that doesn’t need capital from the mother company.

So to sum this up: I think CSU’s business structure can really weather the storm after Mark Leonard stepped down. The whole company was built and organized to not be one-person-focused. It was not like Mark Leonard was signing of on all the acquisitions before he stepped down. And I believe with Mark Miller, they have found an excellent replacement. While no one can replace the charismatic visionary Mark Leonard himself, I think Mark Miller has the experience and knowledge to do very well. Only time will tell.

2.3 AI Impact

This is probably the big one at the moment. All software companies are being heavily sold off due to fears of AI interrupting their business models. In my opinion, these worries are generally overstated, and for CSU in particular. I’ll try to explain what I’ve come to that conclusion in the next section.

I think the big theme around AI disrupting software companies, is that the barrier-to-entry will be a lot lower due to AI advancements and vibe-coding. Software can be easily recreated and improved upon with AI. While I believe the basic premise to be true, I also believe this does not heavily impact CSU’s business model (as of now), as the barrier-to-entry to most of their businesses was already very low to begin with.

These are such niche businesses, that could easily already be disrupted, but the appetite to actually do so has been very low. And I believe it will stay that way.

The TAMs for most of the software companies and markets CSU invests in, is very very limited. They are unlikely to be attacked by bigger firms or companies that are looking to disrupt by using AI. There’s simply not that much money to be gained by doing so. Switching costs for the existing companies using the software, would be very high and let’s not forget, also very inconvenient. The software they have covers their needs (and maybe more), so why would they switch?

Keep in mind, the software is usually mission critical for these companies, and the overall costs are very low, often below 1% of total cost. The risk of losing, or worsening a key program/software for their business is not to be underestimated. Think of it this way: would you change or switch a software-package, just to reduce like 0.2%-1% of your costs, but have the chance to ruin your whole business?

Would you change something that works, that does the job, just to save a few bucks?

And in the meanwhile risk losing a relationship and service that has worked for many years?

AI is also still highly data dependend, it needs a LOT of data to be effective. Most of these so-called disrupting niche software companies lack just that, data. Outsiders simply don’t have the data to interrupt. If anything, the existing companies are way ahead, because they DO have the data needed to train these models, if they ever wish to do so.

Because there is so much discomfort in the software space now, CSU might even have the chance to acquire new businesses at reduced valuations, BECAUSE of these AI threats. PE firms are moving away, valuations are getting cheaper and that might actually open up more possibilities to CSU.

Could AI negatively impact CSU as well, yes of course. We should not close our eyes for this. But I doubt it will be in the near future. Things might progress in a different direction in the long-run, but that’s just something monitor very closely. I believe it is still very hard to predict where AI or AGI will end up in the next couple if years.

Knowing CSU, they will address this during their next AGM, and that should clarify a lot of how they currently view this AI threat. They’ve never shied away from being blunt and honest, and I expect just that in the next AGM.

Mark Miller addressed the AI concern in his latest call in October, here is what he had to say:

After checking in with his business units and customers:

-There didn't seem to be yet any concern about that (AI changing the competitive landscape - and new entrants in the market) so far. One of the things important to note, as always, with our businesses in Constellation, we tend to be fast followers.

Our business leaders, particularly our better business leaders, are usually quick to respond to changes inside of their markets due to moves their competitors make or new entrants make into the market.-

- I've not seen anything, any impact on pace or valuation. Not at all. Stay tuned if there's something else. I haven't seen anything so far-

Will AI have an impact on CSU? No doubt. But the severity of it all seems overblown to be. And the impact CSU will have on the companies they own, by simply implementing AI themselves seems underappreciated.

It’s not like they are gonna sit and wait, and roll-over and let it all happen.

2.4 Limited TAM

The last reason of the recent sell-off is investors are worried about Constellation’s TAM getting limited and their struggle to consistently redeploy FCF at a high IRR. They worry there might not be enough prospects to acquire at interesting valuations. This thought is further supported by the premise that AI might disrupt parts of CSU’s current portfolio, on top of limited the expansion possibilities. A double whammy.

While I think it is undeniable, that it is getting harder and harder for CSU to continue their growth path of the last decade, simply by the sheer volume they have to allocate to maintain their growth, there are still a tremendous amount of companies that are not on CSU’s radar or still have not been acquired. The VMS-market is not yet saturated

In the end, CSU might have to look for different and bigger acquisitions to be able to deploy all their cash. And that could prove to be harder than it seems right now. A bit more on that later in the deep dive.

I would argue negative sector sentiment might even open up more possibilities. As valuation are likely to get cheaper and competitors less interested in the overall market, CSU could step in and take advantage.

Let’s not shy away from being critical, CSU will have to execute very well to keep up with the growth they showed in the recent years, but I believe they can very much sustain their growth level in the next few years, regardless of AI disruptions.

3. Constellation Software as a company

3.1 Definition

So what does Constellation Software actually do. Here is what they say about what they do themselves:

We acquire, manage and build VMS businesses. Generally, these businesses provide mission critical software solutions that address the specific needs of our customers in particular vertical markets.

Our focus on acquiring businesses with growth potential, managing them well and then building them has allowed us to generate significant cash flow and revenue growth. Using a combination of proprietary software and market expertise, we provide software solutions designed to enable our customers to boost productivity, operate more cost effectively, increase sales and improve customer service and satisfaction.

Many of the VMS businesses that we acquire have the potential to be leaders within their particular markets. We target the VMS sector because of the attractive economics that it provides and our belief that our management teams have a deep understanding of those economics.

So, basically they are a so-called ‘‘multi-acquirer’’. They specialize in buying and managing software businesses that develop and maintain vertical market software.

Constellation doesn’t try to micromanage the companies they buy. They are organized into six large Operating Groups), and under those groups are over 1,000 individual business units.

Local managers keep running their businesses. Constellation provides “best practices” and financial coaching but lets the founders and companies run like they used to do.

Their head office is located in Toronto, Canada and they currently have about 64000 employees.

3.2 What is VMS?

VMS is software designed to meet the specific needs of a very particular, niche industry. It targets one specific industry, it usually has very limited competition, a small market size and a high level of customization.

I think a good example is bus scheduling. Think of a system that was specifically built to keep track of where all the buses are and how they should be scheduled. Which ones are due for maintenance or need refueling. There will be absolutely no other use-case for software like this, but it’s a core product for bus companies, and it really helps them to optimize their productivity and keep things running properly.

So, the software is built and used, intensively. But more importantly, it’s built specifically for this niche/sector. Since the TAM (total addressable market) is so small, there’s really no incentive to try to launch new and better software. As long as the current software suffices, there is no need to switch to other new or more fancy software. Of course, the current software needs to be updated and stay relevant enough. But that is what CSU focusses on as well, keeping the current software up-to-date and optimized for their specific use-cases.

The important thing to keep in mind here, there’s almost no upside for new entrants. The TAM is usually not big enough, expansion likely minimal, as the addressable market is usually very stable. We already talked about switching costs, which might be the highest barrier for new entrants to overcome.

HMS is the exact same opposite: that is software that is designed for a wide portfolio of different industries and sectors. Maybe the best example is Microsoft’s Office software. That’s so broad and generic (but good), that it can be used in almost every company in the world. So, general-purpose build, widely applicable and high level of flexibility. The complete opposite of VMS.

3.3 Culture

I think one of the most important aspects of this company is it’s culture and history. The visionary behind all of this, is Mark Leonard. We will go a bit more in-depth into his profile, history and vision for CSU in the next chapter.

For now I want to highlight what he has established in terms of corporate culture, his insights, his foresight, but especially his focus on values and ethics, because this permeates in every corner of the company. This is what makes CSU so unique.

Here are a few company values that really highlight the unique culture within CSU.

Large is not always better: Mark Leonard’s core belief is that large organizations inevitably become bureaucratic and slow. To combat this, he structured Constellation as a collection of over a 1000 independent businesses. Diversifieng like this requires true vision and execution. Not just on a company but also on a personal level. You have to surround yourself with like-minded and equally smart people to pull this of. And Mark Leonard managed to do just that.

CSU is a safe haven: they have famously sold only one business in their entire history (and Leonard publicly expressed regret over it). This “buy and hold forever” promise allows them to acquire companies from founders who care more about their employees’ long-term future than getting the absolute highest bid from a “slash-and-burn” acquirer. CSU is known for being amongst the weakest bidders in take-over ‘‘wars’’. That does not withhold these company owners to still chose for CSU, as they are not looking for just the best price.

Skin in the game: Executive officers are required to invest a large portion of their bonusses (75% of their after-tax bonus) into Constellation common shares (or since 2025 they can also invest in companies they acquire), which are then held in escrow for several years

Down to earth: Mark Leonard’s own personality, which is private, intellectually honest, and avoidant of publicity, has trickled down into the entire company. You notice it in their communication, which is clear and to-the-point. And importantly: non-hyped and self-critical. While one could argue their communication style is boring, I believe it to be very helpful and insightful. They are brutally honest, and don’t shy away from admitting faults and addressing headwinds or difficulties. A good example of this approach is the fact they only do 1 earnings call per year. They believe quarterly calls just provide noise, and do not attribute to their long-term value and approach.

Mark Leonard has built CSU into something that is not focused on day-to-day shenanigans and drained with what some would argue controversial rules and company culture. But the ''boring'' aspect of it, is something I actually really like. What you see is what you get. And there is a lot to like in what you get.

CSU is more focused on execution and living up to core values, rather than dealing with hype and day-to-day market sentiment. They are not trying to influence the stock price, rather the opposite. They are focused on their long-term strategies, and do this by following core principles built on years of excellent leadership and performance.

4. The Management Team

Let's talk management. Because when investing in CSU, you are basically saying: I trust management to allocate capital better then I would be able to do myself. You are not only giving trust to upper management, but you also place trust in the management layers leading the separate operating units.

Before we start with current management, I think we have to talk a bit more about Mark Leonard himself. Because, if you think CSU, you think Mark Leonard.

4.1 Mark Leonard - Founder

Mark Leonard is the visionary behind and the founder of CSU. Mark Leonard’s journey at Constellation Software is the ultimate story of a venture capitalist who decided to stop hunting for “unicorns” and started building an unstoppable army of “workhorses.”

After spending over a decade in the VC world, he realized that small, niche software companies were actually goldmines, but they were being ignored because they weren’t flashy or easy to sell.

So, in 1995, he took $25M and a wild idea to Toronto, founding Constellation with the goal of buying these specialized businesses and, unlike almost everyone else in finance, never selling them.

For nearly thirty years, Mark operated like a “corporate monk.” He became famous for his extreme privacy, refusing to give interviews or pose for photos, which only made his legend grow as the company’s stock price began to skyrocket.

By the time he stepped back from the President role in late 2025 due to health reasons, Mark had turn CSU into a $90B company. Not a bad ROI ha. He proved that you don’t need to be the loudest person in the room to win.

He’s well-known for his annual letters in which he shared his wisdom and vision with the world, showing that patience, discipline, and a genuine love for “boring” software could create one of the greatest wealth-generating machines in history.

Let’s hope he has a speedy recovery and we might see him back in some shape or form someday!

Operating Manual · Colin Keeley")

4.2 Mark Miller - Current CEO

After Mark Leonard stepped down, Mark Miller was appointed as the new CEO. Mark Miller has worked with CSU, and in particular Volaris Group and its subsidiaries for more than 30 years.

He co-founded Trapeze Group in 1988, which was the first company acquired by CSU in 1995. Since joining Volaris Group, Trapeze Group has expanded on a global scale. The focus of his role at CSU has been on growing and developing exceptional leaders, while continuing to acquire great companies that they buy and hold forever

Mark Miller also currently serves on the boards of Lumine Group, Modaxo, ventureLAB and VoxCell BioInnovation.

He has not appeared in many public settings yet, but I think his introduction call last October says all about what he wants to do with CSU. When he was asked the question what he would do differently from Mark Leonard, this was his answer:

I really think it's business as usual. Just continue to push ahead with our existing strategy. I appreciate that sounds like an easy answer, but I think we just continue to push forward, continue to learn, and try to get better at what we're doing within the organization. There's a lot of opportunities to improve how we do capital allocation, operate our businesses. We'll just continue to focus on the same things that we always have here at Constellation in a completely decentralized fashion.

He is not looking to push his own agenda or vision onto CSU. He just wants to continue to do the things they did (because they worked) and improve on them.

He seems like a very straightforward down-to-earth guy as well, just like Mark Leonard. His focus will be on large investments and preparing the company for new leadership in the next decade.

There is not a lot of public information on the rest of the management team. So I’m going to keep it brief and to the point for the rest of them.

4.3 Bernard Anzarouth - Chief Investment Officer

Bernard Anzarouth joined CSU in 1995. He worked closely with the VMS businesses to identify and pursue opportunities for platform and tuck-in acquisitions and to establish licensing or distribution arrangements.

Before joining CSU, Anzarouth was AVP Business Development for Ascom Inc., a Swiss-based technology corporation from 1993 to 1994. Prior to that he held various positions with IBM. He holds a B.Eng. in Electrical/Computer Engineering from McGill University and an MBA from the European Institute of Business Administration (INSEAD).

4.4 Jamal Baksh - Chief Financial Officer

Jamal Baksh has been with CSU since 2003 when he joined as Controller of the Jonas Operating Group. Jamal is currently the Chief Financial Officer. Prior to this role, he served in a number of senior executive roles within Jonas and Constellation including Vice President of Finance for Constellation reporting to the Chief Financial Officer. He is a Certified Management Accountant and holds an Honours Bachelor of Mathematics degree from the University of Waterloo.

4.5 Farley Noble - Senior VP

Farley started with Constellation Software Inc in 1999 and has held CFO and senior M&A roles at head office and operating groups, including Jonas Software and the Volaris Group.

Since April 2021, he has led CSU’s head office Large VMS Investment Group. Farley also took a 2.5 year sabbatical from Constellation between 2019-2021 as the CEO/Co-Founder of a startup in the decentralized investment space. He is a CPA(CA) and holds a Bachelor of Business (Honors) degree from Wilfrid Laurier University.

4.6 Summary

So, to briefly sum this up. Constellation’s team is highly experienced. All board members have been with the company for dozens of years, and have had the chance to incorporate Mark Leonard’s vision into their own business and work ethic.

I believe these people (and many others at CSU) together can fill Mark Leonard’s big shoes. It won’t be easy, but they’ve been trained and seasoned in this business and sector for many years.

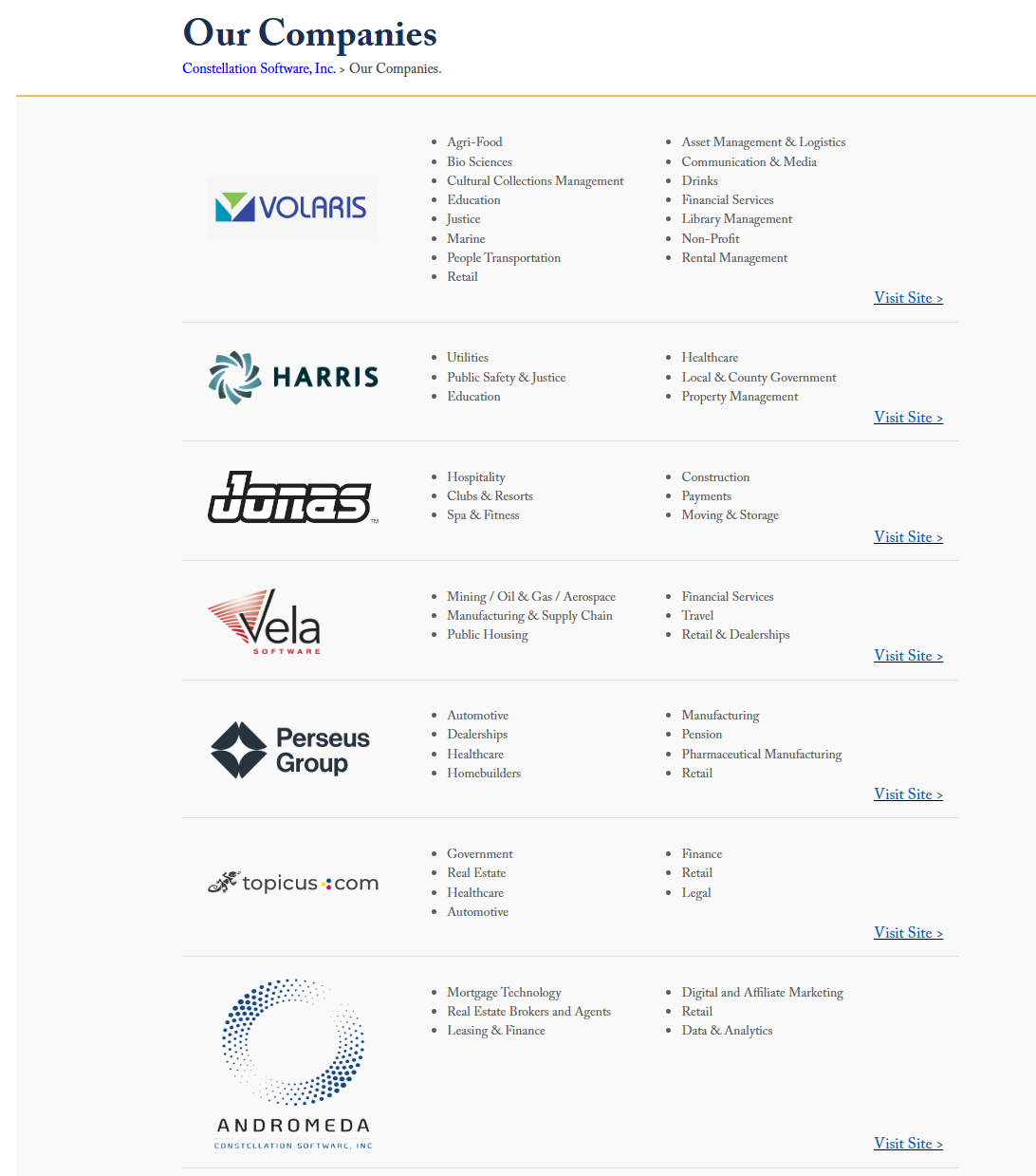

5. Constellation Software’s structure + subsidiaries

So, now we are going to do the tricky thing, try and understand how Constellation’s structure actually really works. As you can see in the picture below, CSU has split themselves into 6 operating groups (excluding themselves).

5.1 The operating groups

The above picture is a bit old, but it does give you a good grasp of how they layers work. I’ll explain in short what all 6 of these operating groups do and what their key focus is. All of these, especially Topicus and Lumine deserve their whole separate deep dives, but I’m not gonna be doing that. I will cover Topicus and Lumine a bit more in-depth in this chapter, but I will still keep it high-level.

Here is a high-level overview of the main focus of all the operating groups.:

Volaris

Volaris focuses heavily on international expansion and diverse vertical markets. They are known for being the “generalist” wing of Constellation, acquiring businesses across more than 40 different verticals.

Their key focus is on: Agri-food, Education, Financial Services, and Asset Management.

Harris

Harris is the oldest operating group and originally focused on the Public Sector. Over time, it has expanded significantly into mission-critical infrastructure software.

Their key focus is on: Utilities (Electricity/Water/Gas billing), Healthcare (Hospitals and large physician practices), and Local Government/Schools.

Jonas

Jonas initially built its reputation in the Club and Leisure markets but has since diversified into over 25 different verticals.

Their key focus is on: Fitness & Sports, Attractions (Theme Parks), Construction, and Foodservice.

Vela

Vela is primarily focused on industrial and asset-heavy sectors. Their portfolio consists of software that helps manage physical resources, manufacturing, and complex global logistics.

Their key focus is on:: Energy (Oil & Gas), Mining, Metals, Manufacturing, and Distribution.

Perseus

Perseus targets businesses that are industry leaders in specialized sectors, often focusing on markets with high stability and long-term customer relationships.

Their key focus is on: Real Estate (MoxiWorks), Mortgage (Optimal Blue), Pulp & Paper, and Finance/Insurance.

Andromeda belongs here with Perseus. Andromeda is not a separate operating group. It remains an operating unit within the Perseus Operating Group for now. They do have their own branding and a distinct mission and focus. Andromeda is particularly active in the mortgage technology and financial services sector.

Topicus

Topicus is unique because it was spun off as its own publicly traded entity in 2021. Its primary focus is the European market, specifically the Netherlands, Germany, and France.

Their key focus is on: Public Health, Social Services, Education, and Financial Services within Europe.

5.2 Why did they do these splits?

Constellation Software’s decision to “split” or spin off certain groups like Topicus and Lumine into separate public companies is a strategic move, and it’s designed to solve the the rapid expansion and the accompanying troubles that came with it.

As Constellation grew, it became harder to maintain high returns on these increasing larger sums of capital. The splits are a way to “reset” the clock and try to maintain their growth engine.

As the they kept buying more and more VMS-businesses, it became impossible for everything to be run and/or approved centrally. By creating separate operating groups, Constellation pushed decision-making closer to operating levels. Each operating group can run its own portfolio of businesses, make smaller acquisition decisions, and allocate capital without constantly going back to head office. This lets the company do many acquisitions in parallel and deploy capital much faster.

The structure also helps preserve the autonomy of the companies Constellation buys. Most acquired businesses are left largely independent, which keeps founders and managers motivated and reduces the risk of damaging customer relationships. The operating groups act as a light governance layer rather than a heavy central bureaucracy.

Another reason is capital allocation discipline. Operating groups effectively compete for capital, with head office allocating funds to the opportunities that offer the best returns. This creates an internal market for capital and reinforces Constellation’s focus on return on investment.

Finally, the split makes the organization manageable at scale. Each operating group is like a smaller version of Constellation itself, with its own leadership and acquisition capability. Spinning off a group also gave the managers an opportunity to take a direct stake in their own operating group. Their bonuses are tied specifically to the performance of their own group, rather than ‘‘mother’’ company where their individual impact might feel diluted and meaningless.

5.3 Topicus.com

So, we have to dive a bit deeper into both Topicus and Lumine. However, I will still keep it very high level, as both these companies kind of require their own deep dive, but that’s not what this CSU deep dive is about.

In early 2021, CSU spun off its European subsidiary TSS (Total Specific Solutions) and merged it with another Dutch company (Topicus B.V.) to create Topicus.com.

CSU has a 30.35% fully-diluted interest in Topicus.

Despite not owning a majority of the common shares, CSU holds a “Super Voting Share.” This gives CSU significant influence over the company’s board and strategic direction.

The ownership is split between CSU, public shareholders, and the original founders of the Dutch Topicus (through an entity called Joday). CSI consolidates Topicus in its financial statements, meaning Topicus is still a key part of the CSU empire.

Topicus is almost exclusively focused on Europe. They capitalize on European fragmentation, different languages, local regulations, and tax laws make it harder for "Big Tech" to compete, creating "moats" around small, local software providers.

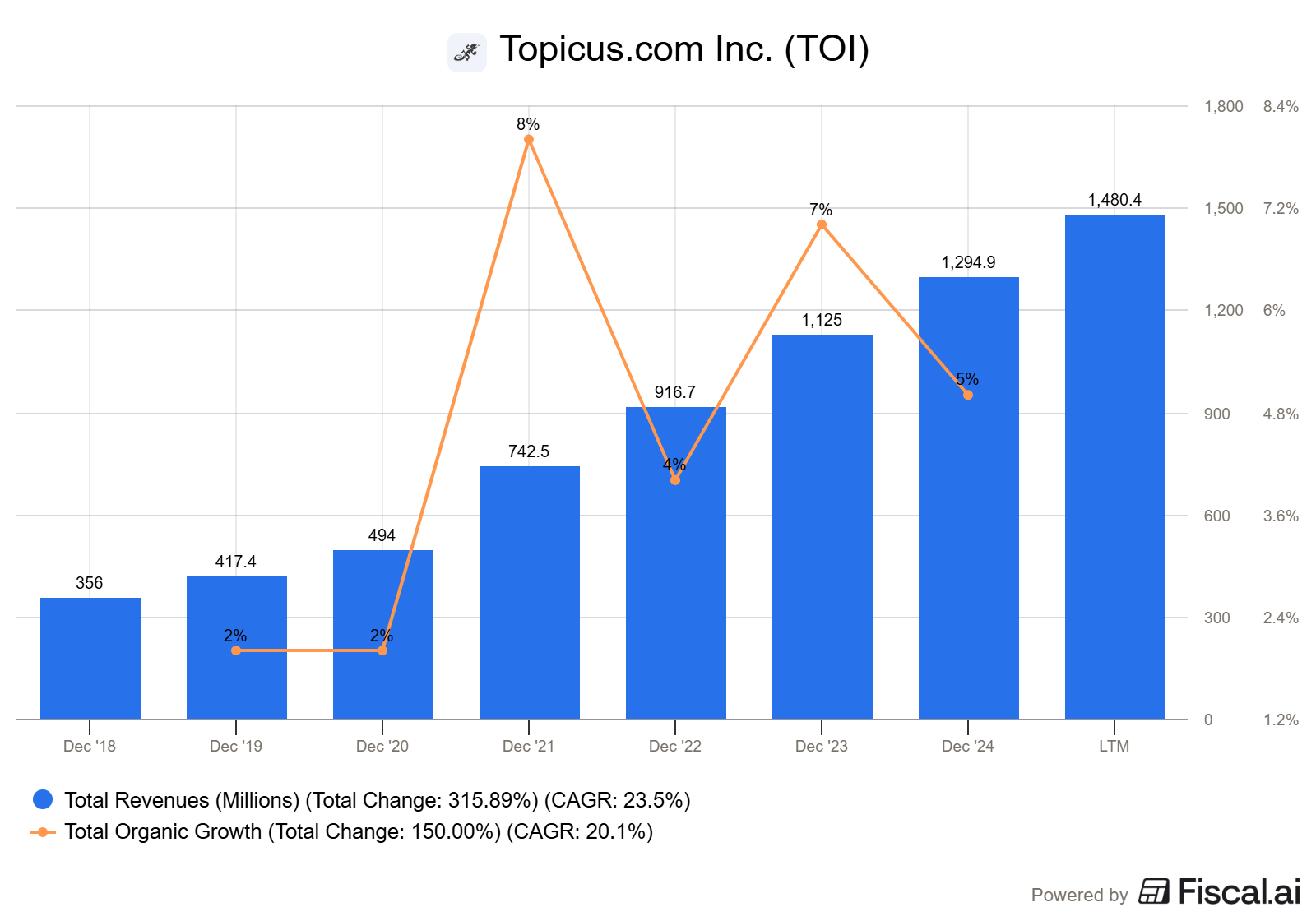

Topicus has delivered consistent double-digit revenue growth in the past quarters, of which about 3%-5% is organic growth, and the rest is revenue growth trough acquisitions. Revenue grew from ~€500M in 2020 to over €1.3B by 2024, continuing to climb in 2025. LTM sits at almost €1.5B.

In 2025 alone, they deployed over €700M in capital, nearly matching their total deployment from the first three years combined. They have grown from roughly 4,000 employees at IPO to over 8,000 today, doubling the size of the business in roughly four years

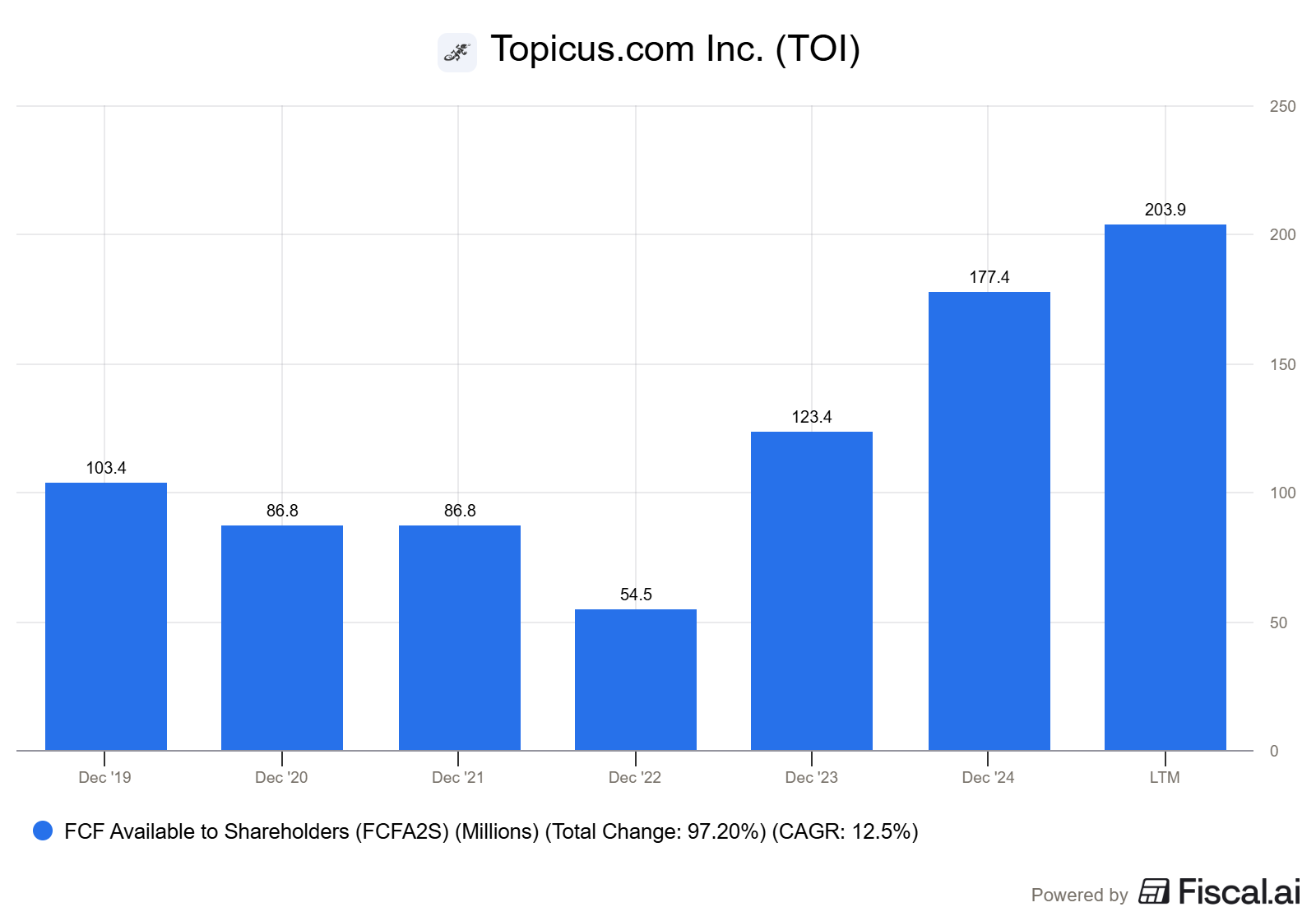

FCFA2S almost doubled since 2019, to about €200M LTM.

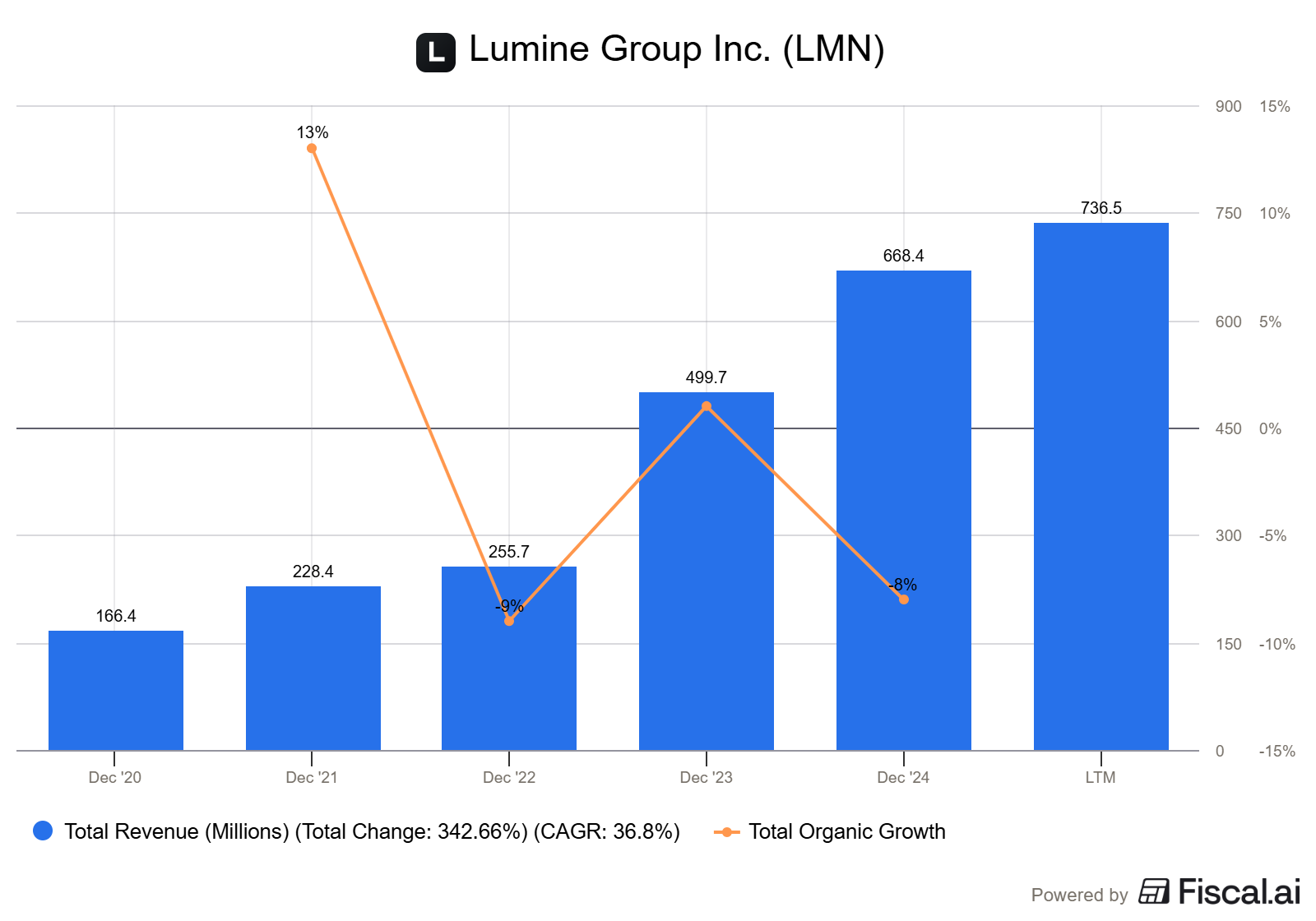

5.4 Lumine

Lumine Group is the second major spin-off from the Constellation Software ecosystem. Lumine is primarily focused on Communications and Media. Lumine was born out of the Volaris Group. Lumine specializes in complex corporate carve-outs. They often buy "orphaned" divisions from giant conglomerates (like Nokia, Ericsson, or Synchronoss) that no longer want to manage a specific software niche.

The spin-off was triggered by the acquisition of WideOrbit, a major U.S. media software firm. To fund the deal and provide a "currency" for future large-scale media acquisitions, CSI carved Lumine out into its own public entity.

Lumine has a complex capital structure where CSI holds Preferred Shares and a Super-Voting Share, allowing them to maintain control and consolidate Lumine’s results while letting Lumine operate independently.

Unlike Topicus, which has very high maintenance/subscription ratios, Lumine deals with more complex systems. This leads to higher initial professional services revenue as they install and customize software for giant telcos. Lumine is deploying capital faster than Topicus did in its early years, specifically targeting larger "platform" deals in the $100M+ range

Revenue jumped from ~$400M pre-IPO to over $1B (LTM) by early 2026, largely due to the WideOrbit merger and subsequent "carve-out" deals. Only a fraction of that is organic growth, which is low but positive around 1%-2%.

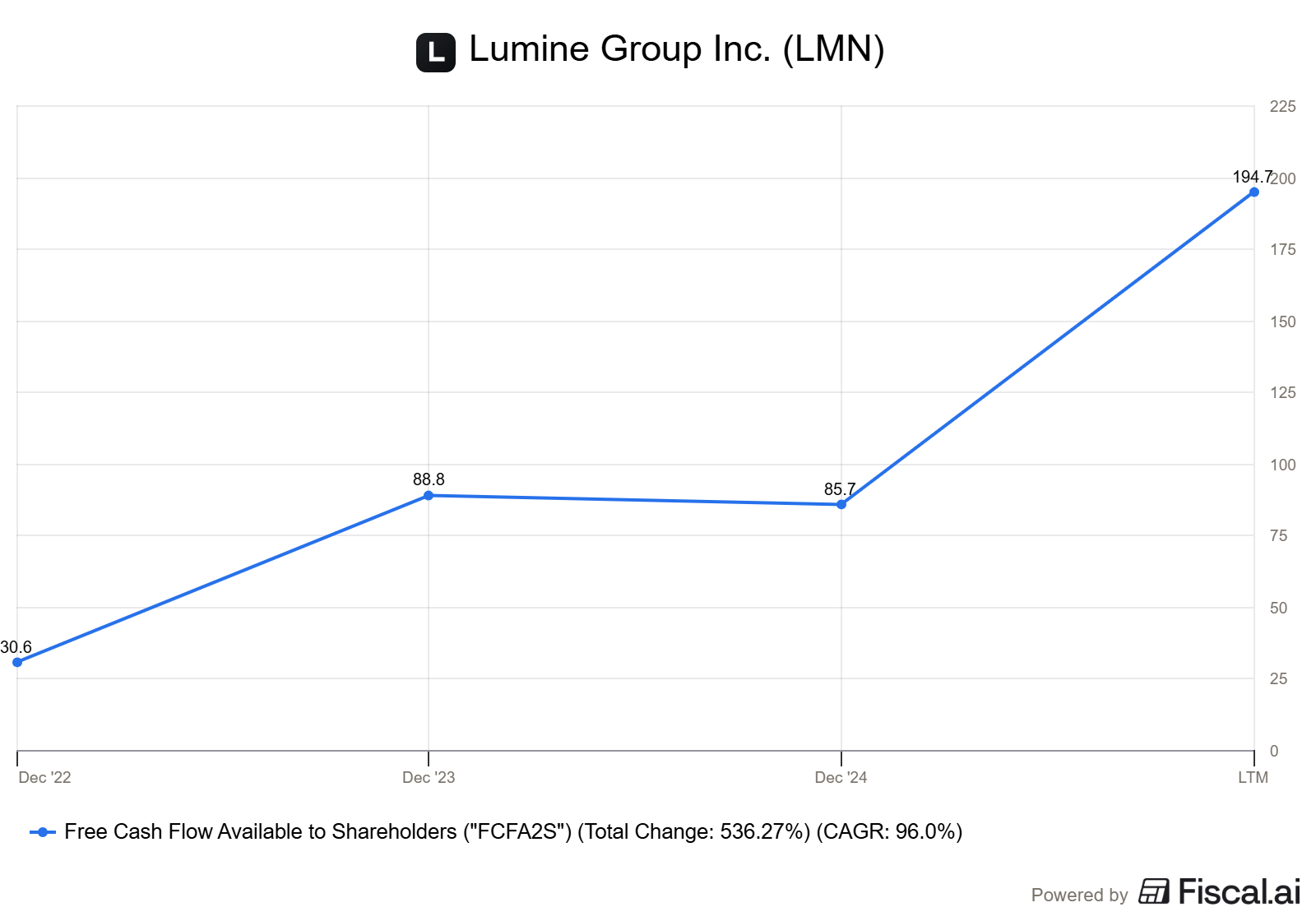

FCFA2S grew over 200% YoY in mid-2025 as the company "cleaned up" the margins of its newly acquired businesses.

6. How does CSU make money?

If you look at CSU in the most simplistic way, it may seem CSU only has one growth strategy: owning and operating vertical-market software companies that throw off recurring cash flow. Everything else is a way of growing or compounding that cash flow.

But it’s a bit more complicated than that, so let’s take a look at the different growth engines we can distinct.